Citadel and Fidelity just made their clearest move yet to rebuild crypto like Wall Street

EDX Markets’ bid for a federal trust bank charter is not just another crypto expansion story. It is a live test of whether Wall Street-backed firms can move more of crypto’s custody and settlement stack inside the U.S. banking perimeter.

Citadel, Fidelity, and Schwab-backed EDX wants to bring equity market structure to crypto through a federal trust bank

EDX Markets’ application for a federal trust bank charter opens a more consequential question than whether another large financial consortium wants deeper exposure to digital assets.

The sharper question is whether some of the firms that helped shape modern U.S. equity market structure are now trying to impose a similar functional separation on crypto, with custody, settlement, collateral management, and fiduciary asset handling pulled into a federally supervised banking perimeter.

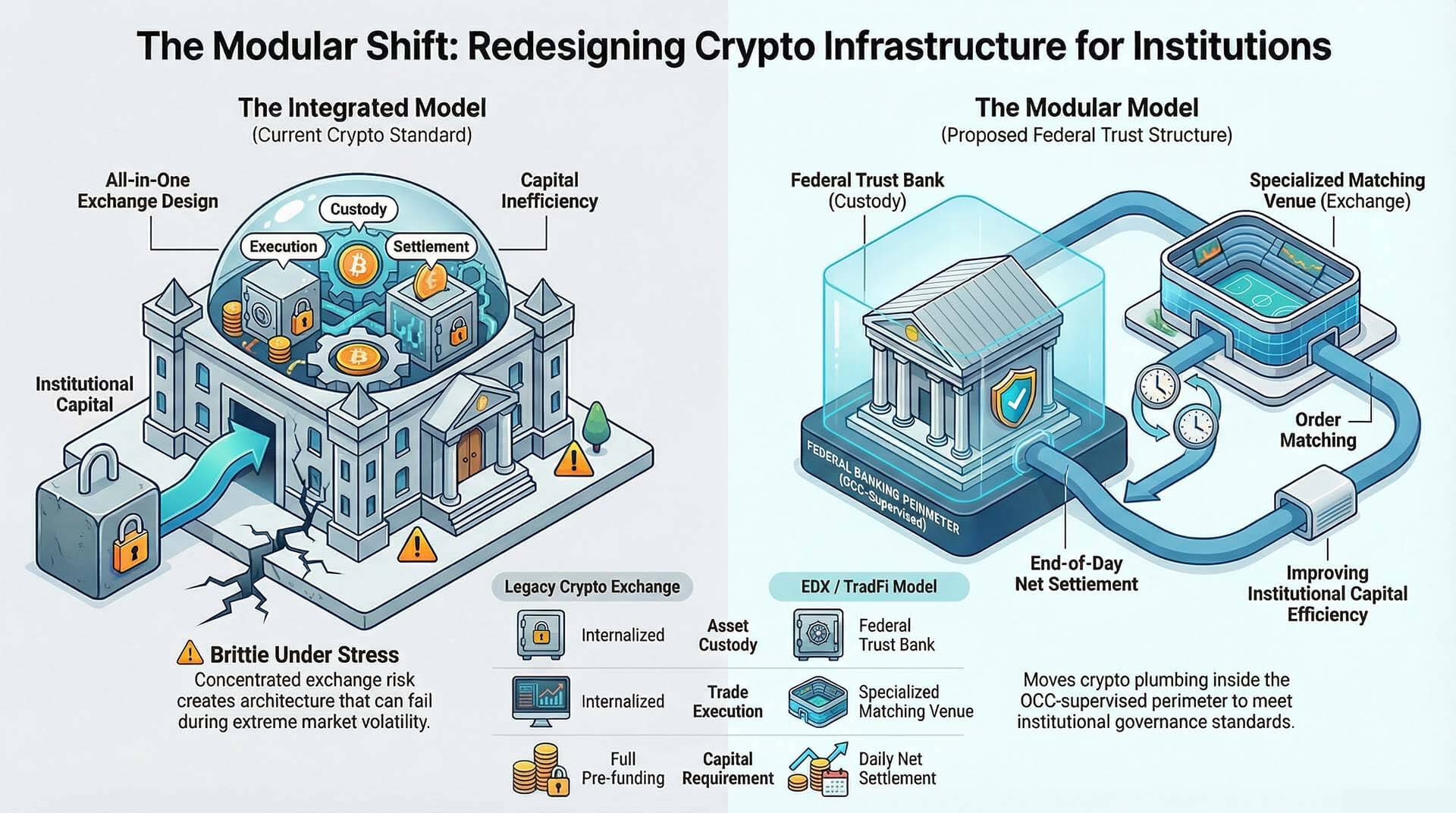

That framing comes directly from EDX Trust’s application to the Office of the Comptroller of the Currency. The filing argues that traditional financial markets evolved around specialized roles, brokers, exchanges, market makers, clearing institutions, and custodians, while digital asset markets developed around vertically integrated venues where execution, custody, and balance sheet functions often sit under one roof.

Why this matters: If this model wins approval and real flow, more of crypto’s back-end infrastructure could move away from all-in-one exchanges and toward federally supervised institutions. That would matter for who controls custody, how trades settle, and which firms become the preferred route for institutional capital.

EDX’s proposal attempts to redraw that map. Order matching would remain with EDX Markets, while the proposed national trust bank would handle custody, fiduciary asset management, settlement-related functions, and riskless principal activity.

For a market still defined by the aftershocks of concentrated exchange risk, that distinction gives the filing its real weight. The application points to a bid to move a meaningful share of crypto infrastructure away from all-in-one venue design and toward a modular structure that institutions already understand.

The names behind EDX add force to that interpretation. Citadel Securities, Fidelity, and Charles Schwab backed the venue at launch, and the proposed trust bank lands at a moment when the federal charter process is starting to look like a competitive lane rather than an isolated regulatory experiment.

The OCC’s digital assets licensing applications page shows that EDX Trust joined a growing queue of pending applicants in March, alongside firms such as Morgan Stanley Digital Trust, zerohash, and Revolut Bank US.

That follows the OCC’s December announcement that it had conditionally approved five digital asset-related national trust bank charters, including applications tied to Ripple, Fidelity Digital Assets, BitGo, and Paxos.

The competitive significance lies in the pattern. Federal trust bank status is starting to look like an emerging layer of institutional crypto infrastructure, one that could shape who gets to intermediate regulated capital and who remains outside the most defensible perimeter.

That gives EDX’s filing a broader significance than a standard custody expansion. The application describes a model built around end-of-day net settlement for spot trades, rather than the heavily prefunded arrangements common across large parts of crypto trading.

EDX argues that this structure could improve capital efficiency and reduce the operational burden on institutional participants. The target users in the filing make the ambition clear: broker-dealers, futures commission merchants, registered investment advisers, corporations, and other regulated intermediaries whose participation depends on custody arrangements, counterparty controls, and supervisory familiarity.

Viewed through that lens, the filing signals an attempt to build a crypto market structure that can carry institutional flow on a larger scale, with federal oversight sitting closer to the assets and the settlement process than crypto venues historically allowed.

Why the filing points to crypto plumbing, not another access story

The most revealing part of EDX’s application is the way it defines the market problem. The document spends far more time on structural separation than on promotional language around adoption or innovation.

That choice says a great deal. EDX is effectively telling the OCC that the missing layer in crypto is infrastructure that regulated institutions can route through without inheriting the operational and governance profile of vertically integrated exchanges.

That argument lands because it maps directly onto how large financial institutions already think about market participation. In equities and listed derivatives, institutions operate through a web of specialized actors and clearly delineated responsibilities.

Matching venues match. Custodians custody. Clearing and settlement functions sit in distinct frameworks. Risk is measured and transferred across known institutional channels.

Crypto still looks uneven by that standard. Exchanges often combine execution, asset custody, financing, and internal balance-sheet activities. The result is an architecture that can scale quickly in bull markets but looks brittle under stress.

EDX’s proposed trust bank aims to answer that structural gap. According to the application, EDX Trust would provide custody for digital assets and fiat balances, fiduciary asset management, and settlement support for spot transactions executed on EDX Markets.

The filing also states that custodied cash and stablecoins would be invested in highly liquid instruments targeting returns near the federal funds rate, while custodied digital assets could be staked or used in permissible yield-generating activities. That broadens the institution’s role beyond safekeeping. It places the proposed bank closer to the center of collateral, idle asset utility, and balance-sheet efficiency.

Settlement design sits at the center of the pitch

The settlement design is especially important. EDX states in its OCC application that spot trades would settle once per day on a net basis and that certain clients could post collateral rather than fully prefund activity, depending on their financial condition and risk profile.

That departs from one of crypto’s defining constraints, the need to warehouse capital across venues in advance of execution. For active institutional participants, capital efficiency directly affects how much flow can move, how much inventory must sit idle, and whether participation scales beyond exploratory allocations.

This is where the EDX model starts to look like an effort to import the habits of mature market structure into crypto. The firms behind the venue understand fragmented liquidity, specialized roles, and the economics of execution architecture at a very high level.

Their filing reads like a view that crypto can no longer rely on venue-centric design to sustain institutional depth. Vertically integrated exchanges may continue to command large volumes, though a federally chartered trust layer could become the preferred route for some classes of institutions that have held back or participated only through narrow channels.

A second signal sits in the way EDX handles custody itself. The application says the proposed bank would use sub-custodian banks to hold private keys. That introduces another layer of segregation and operational specialization.

It also reinforces the idea that the filing is trying to carve clear boundaries around function, liability, and control. As those boundaries harden, crypto infrastructure starts to resemble the institutional layouts that dominate traditional capital markets.

The next test is whether institutions move flow, and whether charter status becomes a durable moat

The federal charter itself will draw attention, though the more durable question is whether this model attracts real institutional migration. Regulatory approval would establish legitimacy and supervisory footing.

On its own, approval would still leave open the commercial question of whether the architecture wins flow. Institutions will need to decide whether the combination of a matching venue plus a federally supervised trust-bank layer offers a superior route for execution, custody, capital efficiency, and governance compared with incumbent crypto venues and existing bilateral arrangements.

There are reasons to think that the question is now live. The OCC’s December conditional approval for Fidelity Digital Assets’ conversion to an uninsured national trust bank showed that the federal banking perimeter is already opening to crypto-native and crypto-adjacent infrastructure.

Fidelity’s approval contemplated crypto custody and trade execution services, creating a notable benchmark within the broader shareholder ecosystem surrounding EDX. At the same time, the OCC’s current application queue suggests several firms see strategic value in securing the same kind of status.

Once multiple players pursue the same charter path, charter access starts to resemble a competitive boundary rather than a badge.

That competitive boundary could reshape the exchange landscape. If custody, settlement, and collateral functions migrate toward federally chartered trust institutions, then the economic center of gravity in crypto could shift away from venue-centric models and toward modular infrastructure.

A venue would still matter for liquidity, matching quality, market design, and access. Yet the parts of the stack that institutional allocators care about most, asset control, segregation, supervisory clarity, and settlement discipline, could move into entities built specifically for those functions. That would pressure the long-standing logic of keeping everything under one roof.

EDX also enters this phase with some scale history behind it. According to Ledger Insights, which cited company figures, EDX processed $36 billion in cumulative notional trading volume during 2024.

That number should be treated as company-reported rather than independently verified market share, though it still provides a useful reference point. It suggests EDX is filing from a position of operational experience, rather than concept alone.

The venue expanded its listed assets well beyond its initial launch lineup. The operating premise is clear. EDX wants a broader product scope paired with a structure designed to carry larger institutional participation.

The unresolved part sits in adoption. Large intermediaries and asset managers will need to decide whether a trust-bank-based structure genuinely improves the economics and controls of participation.

Market makers will need to assess whether the model supports the same depth and responsiveness they require. Institutions that already route activity through crypto-native venues will weigh operational familiarity against the appeal of federal supervision and stronger functional separation.

That comparison will determine whether this filing marks a structural pivot point or merely another incremental layer in crypto’s long regulatory buildout.

For now, the signal is still strong. EDX’s application frames crypto’s institutional bottleneck as a market-structure problem and proposes a federal trust bank as part of the solution.

That puts the next phase of competition in a different place. The market has spent years focused on products, access points, and the expansion of listed assets. The more consequential contest may now sit deeper in the stack, where custody, settlement, collateral management, and supervisory architecture determine who can intermediate the next wave of institutional flow, and on what terms.

The post Citadel and Fidelity just made their clearest move yet to rebuild crypto like Wall Street appeared first on CryptoSlate.