MSTR stock is beating Bitcoin, but another Strategy asset matters more now

Throughout 2026, MSTR stock and Strategy’s preferred securities are trading as more than a simple Bitcoin proxy.

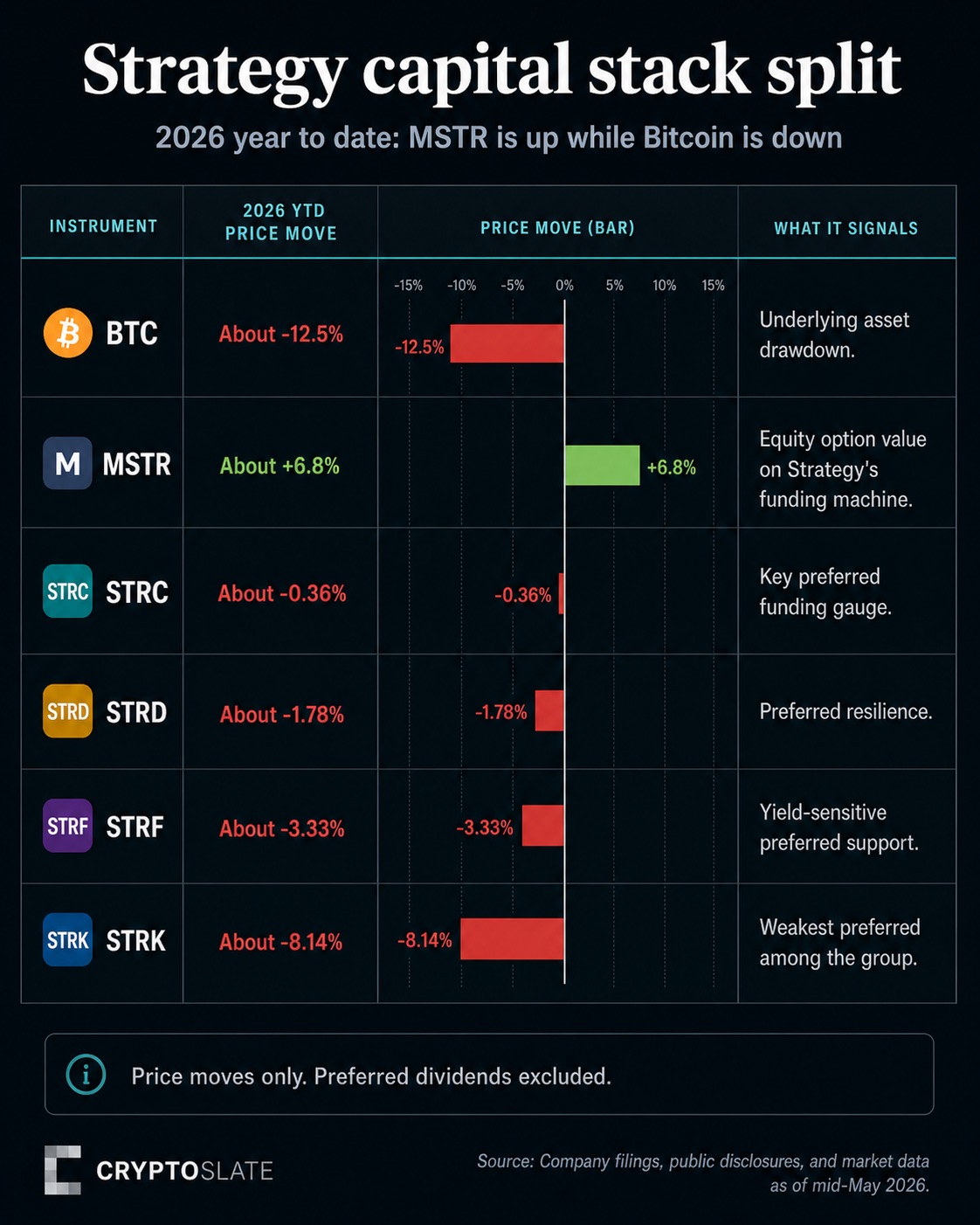

Bitcoin is down about 12.5% year to date, while Strategy stock, trading as MSTR, is up about 6.8%

Strategy's preferred securities have also held up better than BTC in price. STRC is nearly flat, while STRD, STRF, and STRK have all shown smaller price declines than spot Bitcoin. Those preferred figures are price moves and exclude dividends.

The split shows investors valuing two separate parts of Strategy's model: the common stock's exposure to Bitcoin plus capital-markets execution, and the preferreds' claim on dividend confidence, collateral coverage, and the durability of the funding channel.

| Instrument | Year-to-date price move | What it signals |

|---|---|---|

| BTC | About -12.5% | The underlying asset drawdown |

| MSTR | About +6.8% | Equity option value on Strategy's funding machine |

| STRC | About -0.36% | Preferred demand and repeatable funding near par |

| STRD | About -1.78% | Preferred resilience with credit and yield sensitivity |

| STRF | About -3.33% | Yield-sensitive preferred support |

| STRK | About -8.14% | The weakest preferred among the group, with more equity-linked sensitivity |

Within Strategy's investment complex, MSTR has delivered the strongest realized price move so far. STRC is the better risk-adjusted asset for the rest of 2026 because it is the live test of whether preferred buyers will keep financing Strategy's Bitcoin purchases without demanding deeper price concessions.

How the tickers fit together: MSTR is the common stock, the high-beta expression of Strategy's BTC balance sheet, and its ability to keep raising capital at a premium. STRC is a par-anchored preferred stock that has become the most important 2026 funding gauge. STRF and STRD appear more credit- and yield-sensitive, while STRK carries more equity-linked sensitivity. Note: The legacy MicroStrategy stock search term still points investors toward the same Strategy equity trade.

That structure explains why the group can move in different directions. MSTR reacts to Bitcoin, the company's net asset value premium, and the market's confidence in future issuance. The preferreds react more directly to whether investors trust the dividend stream, the collateral cushion, and Strategy's ability to keep the funding channel open.

MSTR is pricing more than Bitcoin exposure

MSTR's strength is striking because, in a simple model, its common stock should be highly exposed to Bitcoin. Strategy's balance sheet is dominated by BTC, and its equity is the highest-beta part of the stack.

If the market were treating MSTR purely as a BTC wrapper, a double-digit Bitcoin decline would normally pressure the common stock.

MSTR's gain suggests investors are pricing a second layer: Strategy's execution premium.

The company is holding BTC and using public equity and preferred stock markets to turn investor demand for yield, convertibility, or leveraged Bitcoin exposure into fresh purchasing power.

That distinction is central to the vehicle choice. MSTR gives investors the highest-beta expression of Strategy's BTC balance sheet and the strongest upside to a durable premium.

It also carries the clearest downside if that premium fades, because the common equity is where expectations for repeated issuance, accretive purchases, and market confidence meet.

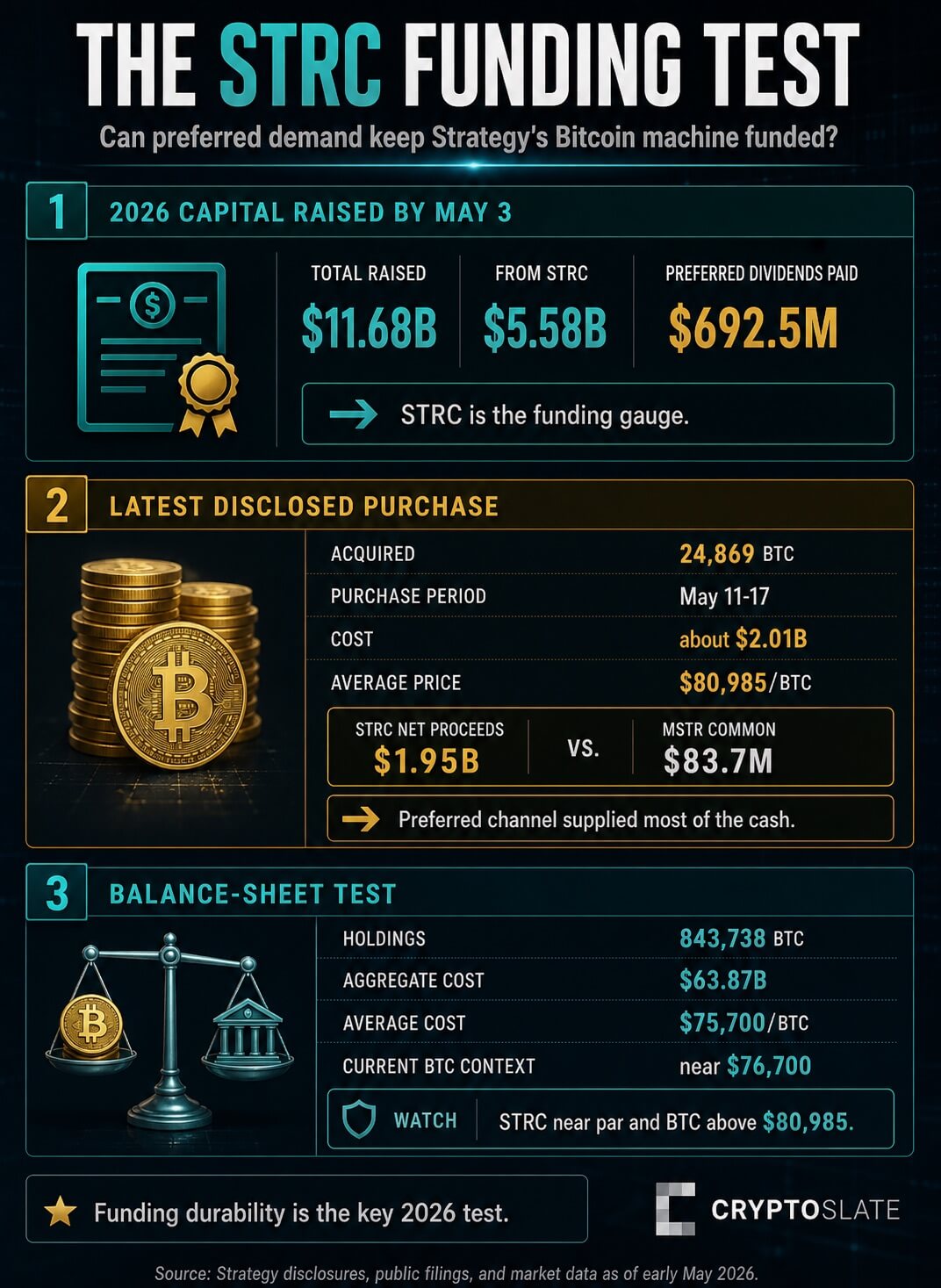

Strategy's Bitcoin count keeps rising. The company's purchase table shows holdings of 843,738 BTC as of May 18, up from 672,500 BTC on Dec. 31, 2025.

That is an increase of 171,238 BTC year-to-date. The same table shows an aggregate acquisition cost of $63.87 billion and an average cost of $75,700 per BTC.

That scale helps explain why MSTR can trade differently from Bitcoin itself.

The stock is exposed to BTC price, but it also reflects whether markets believe Strategy can keep issuing capital above the value of its Bitcoin holdings, buy more BTC during weak periods, and preserve a premium to its BTC net asset value.

The risk is that the same mechanism can become less efficient.

If the equity premium compresses, common issuance becomes less attractive. If preferred buyers demand a wider discount or a higher yield, the capital machine still operates with greater friction.

MSTR's outperformance is the strongest evidence for Strategy's access to public markets. For spot BTC, support is indirect and depends on incremental buying enabled by the funding channel.

STRC is the more direct funding gauge

The preferreds are sending a quieter message than MSTR. They have outperformed Bitcoin by price year to date, yet they have not captured the common stock's upside.

That is defensive behavior in the year-to-date comparison, with each preferred still tied to dividend confidence, collateral coverage, and funding durability.

STRC is the key instrument because it is close to par, has become a major funding channel, and sits at the center of Strategy's 2026 issuance.

Strategy said it raised $11.68 billion through capital markets activity year to date as of May 3, including $5.58 billion from STRC.

That makes STRC more than another ticker in the stack. It is a market referendum on whether investors still want to fund Strategy's Bitcoin strategy through preferred stock. That makes the Strategy Bitcoin trade a funding question as much as a balance-sheet question.

The May 18 filing made that point clearer. Strategy reported that it acquired 24,869 BTC over May 11-17 for about $2.01 billion at an average price of $80,985 per BTC.

For the latest disclosed purchase period, Strategy raised roughly $1.95 billion of net proceeds from STRC, compared with $83.7 million from MSTR common stock.

That mix means the latest disclosed purchase was funded primarily through the preferred channel.

For Bitcoin holders, that creates incremental demand. For Strategy holders, it also creates a liability and confidence test.

Preferred capital has a cost, and Strategy said cumulative dividends declared and paid on all preferred stock reached $692.5 million as of May 3.

That makes the preferred comparison a price-return snapshot, rather than a complete total-return ranking. Preferred dividends would need to be included before comparing their full investor return with MSTR or spot BTC.

Those distributions are also the carrying cost Strategy must keep servicing as the funding stack grows.

STRF and STRD appear more tied to credit and yield confidence. STRK, which has fallen more than the other preferreds year to date, has greater equity-linked sensitivity.

STRC's near-flat price is important because it is the instrument closest to the current funding question: can Strategy keep selling a par-anchored preferred at terms that make new Bitcoin purchases look accretive?

The newest Bitcoin has little cushion

The funding question is tied to Strategy's purchase prices. The full Bitcoin stack sits near its aggregate cost basis, while the newest disclosed purchase was made above the current BTC price context used here.

Strategy's full Bitcoin stack, at an average cost near $75,700, is close to the current Bitcoin market context.

CryptoSlate's Bitcoin price page showed BTC near $76,700, while the broader crypto market was around $2.56 trillion with BTC dominance near 60.1%.

That leaves the aggregate position with a modest cushion. The newest capital has less room.

The May 11-17 purchase price of $80,985 is above the current BTC price context, around $76,700. If Bitcoin stalls below that purchase price, the newest tranche can look stretched even while the full stack remains near its aggregate cost basis.

This is the core tension behind the capital-stack outperformance.

Strategy is still accumulating BTC at scale during a drawdown, which can support the bullish case around institutional-style demand for Bitcoin.

The same facts raise the funding test. If BTC fails to rebound, preferred investors must remain confident in collateral coverage, dividend durability, and the company's ability to convert market trust in refinancing into Bitcoin purchases.

Prior CryptoSlate coverage has already framed STRC as part of Strategy's preferred-stock funding loop and questioned whether large Strategy purchases continue to serve as straightforward bullish catalysts for BTC.

Note: The MicroStrategy Bitcoin frame still describes the same core issue: equity and preferred markets are financing incremental BTC accumulation.

The 2026 divergence extends that point. Public markets are separating the equity option, the preferred funding channel, and the underlying asset.

For realized performance, the answer is MSTR. It is the clear winner year to date, rising while Bitcoin fell and while the preferreds mostly defended rather than rallied.

For the rest of 2026, the more useful signal is STRC.

If STRC can hold near par and continue absorbing issuance, Strategy's funding window remains open. That keeps the company positioned to buy Bitcoin into weakness and sustain the premium narrative embedded in MSTR.

If STRC trades persistently below par or requires more expensive terms, the machine becomes less efficient, even if Strategy can still raise capital.

That makes the divergence mainly bullish for Strategy's capital-markets machine. It is selectively bullish for Strategy because MSTR is still receiving credit for issuance capacity and execution.

For Bitcoin, the support is indirect: it depends on the funding channel staying open and on the new purchases eventually looking accretive.

The next test is whether STRC remains a repeatable funding channel while BTC is below the newest purchase price.

A move back above $80,985 would make the May 11-17 tranche look cleaner. Continued trading near the aggregate cost basis would keep the debate alive.

A deeper BTC decline, paired with sustained below-par preferred pricing, would turn the capital-stack split from a sign of resilience into a stress test of Strategy's 2026 model.

The post MSTR stock is beating Bitcoin, but another Strategy asset matters more now appeared first on CryptoSlate.