New Coinbase CLARITY Act standoff over stablecoin reward is now holding up rules for the entire US crypto market

The stablecoin yield fight has once again consumed the CLARITY Act debate on Capitol Hill, and the cost of that consumption is now measurable.

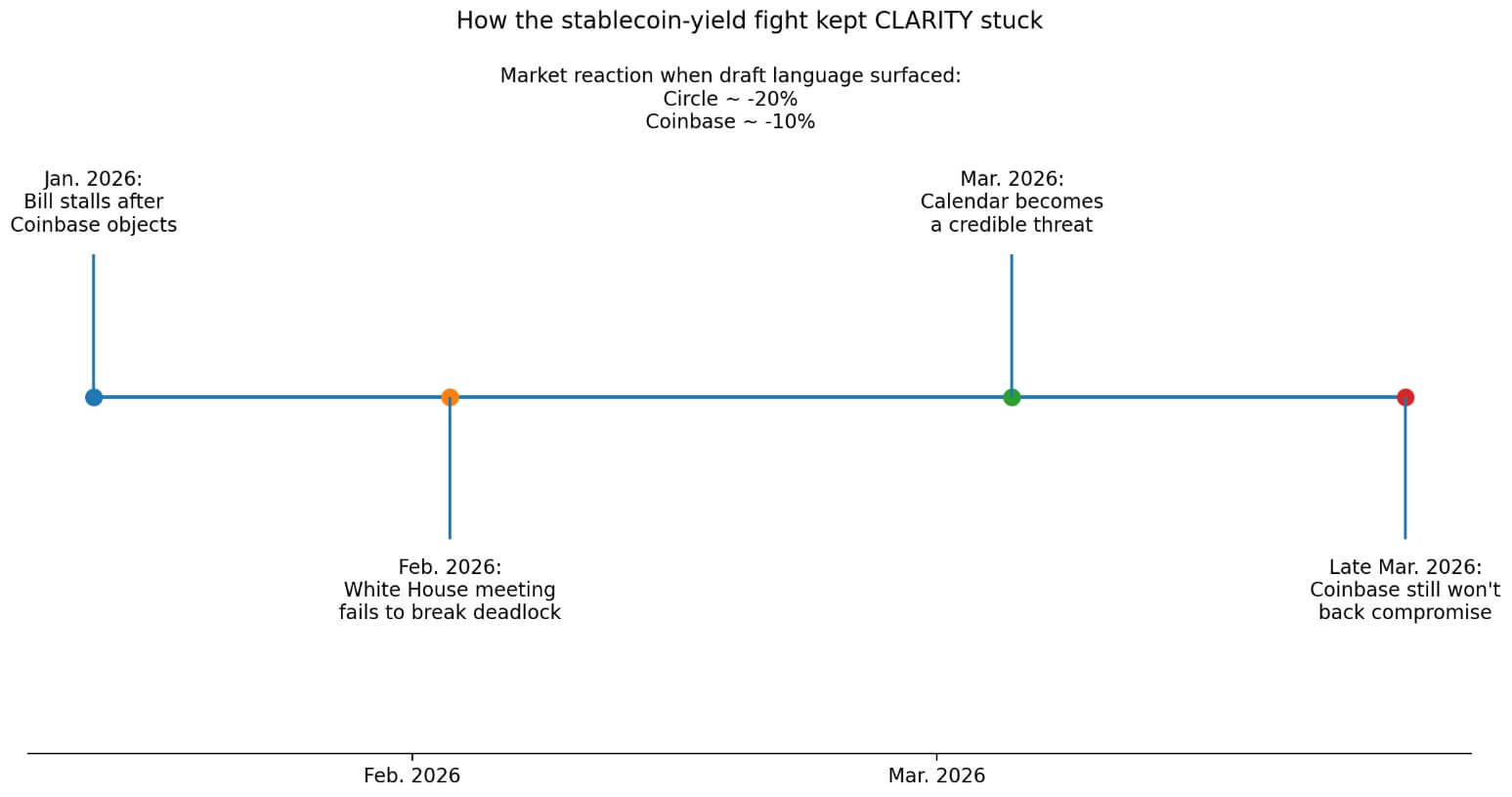

The bill stalled in January when Coinbase objected to its terms, a White House meeting in February failed to break the deadlock, and by March, the calendar itself had become a credible threat to passage.

Punchbowl’s latest report suggested Coinbase representatives told the Senate they still could not support the newest stablecoin-yield compromise. But the signal is less definitive than January’s break: Brian Armstrong has not publicly restated his opposition to the new text, and White House crypto adviser Patrick Witt dismissed claims that Coinbase was once again blocking the bill as “uninformed FUD.â€

That leaves the live question slightly narrower than a full industry walkout: whether the latest rewards language is still too restrictive to hold the coalition together on a bill whose stakes run far beyond yield.

Banks want CLARITY to close what they see as a loophole in last year's stablecoin law that lets exchanges pay passive rewards on idle balances. Crypto firms argue that banning rewards is anti-competitive and weakens user acquisition.

Circle fell roughly 20%, and Coinbase about 10% when draft language surfaced that would bar passive stablecoin rewards, indicating that markets are pricing this fight aggressively.

The fight concerns just one product feature in one class of balances. CLARITY's reach extends across the entire US crypto operating environment.

The jurisdictional prize

In January, reports noted that the Senate bill would define when tokens are securities, commodities, or otherwise, and grant the CFTC authority over spot crypto markets.

Senate Banking Republicans describe this as drawing a “bright line†between the SEC's and the CFTC's jurisdiction, ending the enforcement-by-litigation regime that has governed token classification for years.

The House-passed framework assigns the CFTC core authority over registered digital commodity exchanges, brokers, and dealers, as well as spot market contracts of sale.

That jurisdictional settlement underpins exchange listings, token distribution, institutional custody decisions, and the legal posture of every crypto firm operating in the US today.

Section 202 of the House-passed text creates an exemption from traditional securities registration for qualifying digital commodity offerings, provided issuers meet disclosure requirements.

Sections 203-205 govern secondary market treatment, insider and affiliate sales, and the point at which a blockchain network qualifies as sufficiently “mature†to exit securities classification.

Senate Banking Republicans frame this as a purpose-built disclosure regime that lets responsible projects raise capital while protecting investors.

For the next generation of builders, access to a lawful US fundraising path carries more long-run weight than any reward rate on a stablecoin balance.

| Area | What CLARITY would do | Why it matters |

|---|---|---|

| SEC vs. CFTC jurisdiction | Draws a statutory line between when tokens fall under securities oversight and when they fall under digital commodity oversight, while giving the CFTC authority over spot crypto markets | Determines who regulates tokens, exchanges, and spot trading, replacing years of ambiguity and enforcement-driven classification |

| Token fundraising path | Creates a disclosure-based exemption for qualifying digital commodity offerings and sets rules for secondary-market treatment, insider sales, and when a network is considered “mature†| Gives projects a lawful U.S. path to raise capital instead of pushing token formation offshore |

| Developer and DeFi protections | Excludes certain activities such as validating, node and oracle operation, publishing or updating software, developing wallets, providing user interfaces, and publishing blockchain systems from being treated as regulated intermediation | Narrows legal risk for builders and draws a clearer line between writing code and operating a financial intermediary |

| Self-custody and peer-to-peer rights | Preserves the right of individuals to use hardware or software wallets for lawful self-custody and to engage in lawful peer-to-peer digital asset transactions | Protects basic ownership and usage rights that many in crypto view as foundational |

| Centralized market plumbing | Requires exchanges, brokers, and dealers to register, meet capital and risk-management standards, segregate customer funds, follow surveillance and disclosure rules, and use qualified custodians | Creates the operational and custody framework institutions need before expanding U.S. crypto participation |

Developers, interfaces, and the code-versus-control line

Sections 309 and 409 of the House-passed bill exclude certain DeFi-related activities from SEC and CFTC regulation, while preserving anti-fraud and anti-manipulation authority.

The protected list includes validating, node and oracle operation, publishing and updating software, developing wallets, providing user interfaces, and publishing blockchain systems.

Senate Banking Republicans summarize the philosophy as regulating control. That framing carries direct weight for developers now operating under genuine criminal ambiguity.

A jury convicted Roman Storm in August 2025 on one count of conspiracy to commit an unlicensed money-transmitting business, tied to Tornado Cash. It deadlocked on the money laundering and sanctions counts.

Prosecutors sought a retrial on the remaining charges.

Storm's prosecution runs on a legal track governed entirely by existing law and alleged conduct predating any statutory reform.

A statute that treats publishing software and operating interfaces as protected activity would draw a different line from the one prosecutors used in that courtroom, shaping the legal exposure of the next developer facing a similar question.

The House report states that a US individual retains the right to maintain a hardware or software wallet for lawful self-custody and to engage in direct peer-to-peer digital asset transactions for lawful purposes, subject to sanctions and illicit-finance limits.

Senate Banking Republicans separately confirm the bill preserves self-custody. That provision addresses a foundational question about American crypto ownership that only a statute can settle with durability across administrations.

The plumbing that institutions actually need

Registered digital commodity exchanges under CLARITY would have to meet listing standards, trade surveillance obligations, conflict-of-interest rules, and system safeguards. They could list only assets with public disclosures covering source code, transaction history, and asset economics.

Brokers and dealers would register, meet capital and risk-management standards, segregate customer funds, and hold customer digital assets with qualified custodians.

This is the layer of market infrastructure that large asset managers need before expanding their US crypto exposure beyond already-approved ETF structures.

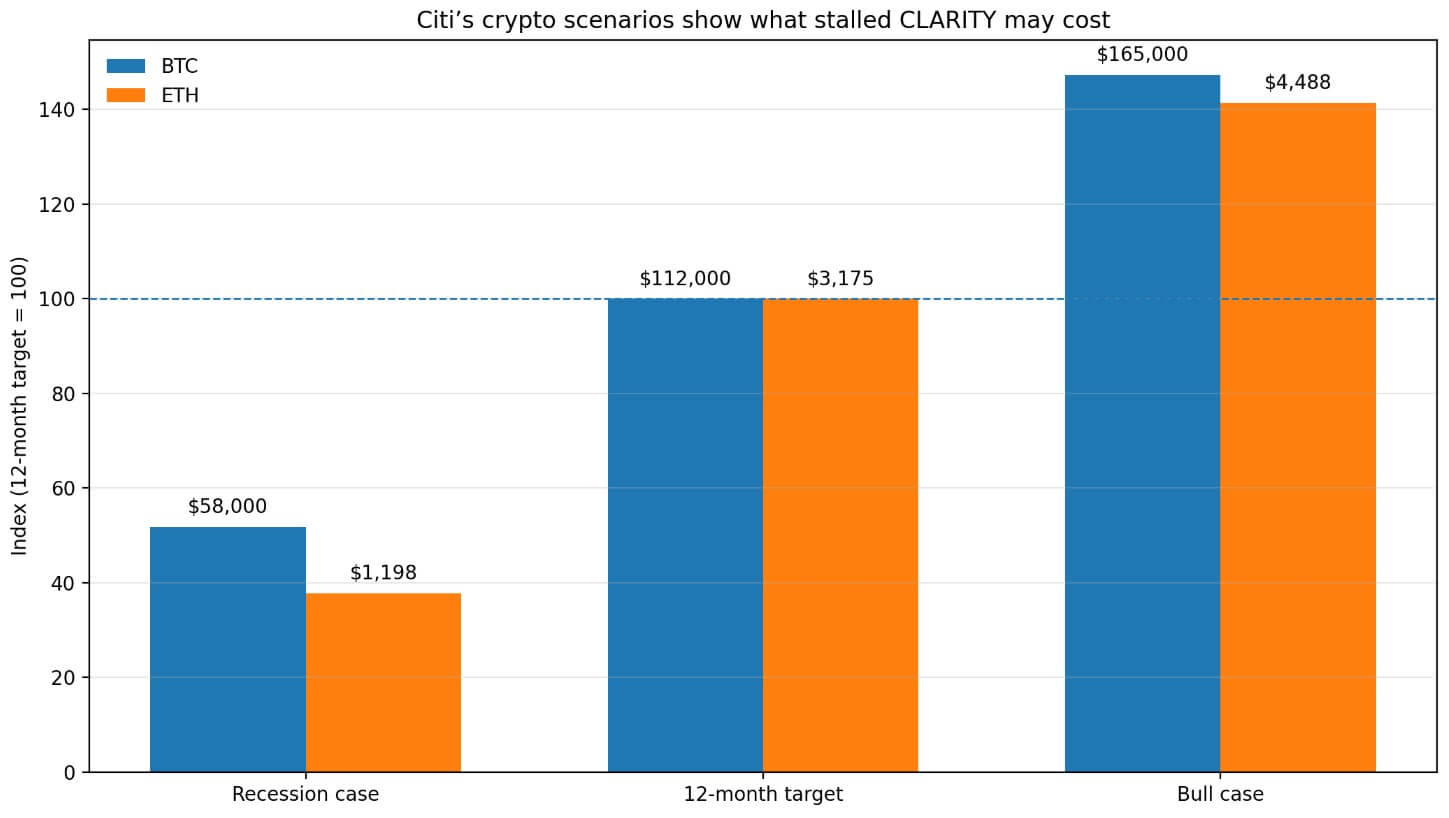

Citi cut its 12-month BTC target to $112,000 from $143,000 and its ETH target to $3,175 from $4,304 in March, citing stalled US market-structure legislation and a narrowing window for the regulatory catalysts required for institutional adoption.

Citi's bull case kept BTC at $165,000 and ETH at $4,488, and its recession scenario put BTC at $58,000 and ETH at $1,198.

That spread between outcomes reflects exactly what CLARITY was supposed to compress: the uncertainty premium embedded in US token classification, exchange oversight, and institutional access.

Without a durable statute, the industry continues to operate under agency guidance that shifts with administrations.

What to expect

A bullish conclusion includes the yield fight finding a workable compromise before Senate floor time evaporates. With that veto point cleared, enough Democrats join the coalition, and CLARITY reaches a final vote in 2026.

The market consequence runs directly through Citi's bull-case math: statutory SEC/CFTC lines revive the regulatory-catalyst narrative, giving institutional allocators the legal certainty to expand positions.

Projects launch US token offerings under Section 202, developer liability narrows to conduct alone, and self-custody protections are embedded in federal law.

On the flip side, passive rewards and activity-based rewards could stay irreconcilable. Senate floor time would then bleed into ethics disputes, cross-committee reconciliation fights, and the midterm calendar.

Congress then approaches the elections without a finalized package, and crypto continues to operate under enforcement history, partial agency guidance, and administration-dependent signals.

As a consequence, the developer-liability question remains open, the SEC/CFTC boundary remains contested, projects continue to route capital raises offshore, and self-custody rights remain unprotected by statute.

The yield fight consuming CLARITY's legislative window blocks the legal architecture that would govern who regulates tokens, how builders raise money, whether developers face criminal exposure for publishing code, and whether Americans can hold their own assets without federal ambiguity.

Yield is still the clearest operational choke point, but it is no longer the bill’s only drag. Democrats involved in the talks have also pushed conflict-of-interest and personal-profit concerns tied to Trump-linked crypto activity, adding another source of delay as the legislative window tightens.

The post New Coinbase CLARITY Act standoff over stablecoin reward is now holding up rules for the entire US crypto market appeared first on CryptoSlate.