Venice’s $65M raise makes VVV holders ask how much of Venice’s growth reaches the token

Venice, the AI platform behind the VVV token, raised $65 million in a Series A led by Dragonfly at a $1 billion equity valuation, its first outside capital raise. The company chose stock over its own token, and the market is already arguing about what that choice means for VVV holders.

Series A investors received 8.98% equity, a 1.5 million VVV vesting grant, and warrants to purchase 5 million additional VVV over 8 years. That package brings together Dragonfly, Coinbase Ventures, North Island Ventures, and other participants on both sides of Venice's capital structure, with equity and tokens held in the same deal.

| Holder group | Asset held | What they get | Key limitation |

|---|---|---|---|

| Series A investors | 8.98% equity, 1.5M VVV grant, warrants for 5M VVV | Legal ownership in Venice AI plus token-linked upside | Token exposure vests over time and depends on market demand |

| VVV holders | Public token | Staking access, DIEM minting, exposure to buy-and-burn mechanics | No direct legal ownership of Venice AI |

| Venice treasury | 30M+ VVV | Largest token position; alignment with public VVV holders | Treasury value depends on VVV market price |

| Venice AI equity holders | Company stock | Corporate upside, ownership rights, contractual protections | Not publicly liquid like VVV |

| DIEM users | Compute credit minted through VVV staking | $1 of daily-renewing Venice compute access per DIEM | Utility exposure, not ownership exposure |

Venice's own VVV page describes the token as a long-term deflationary capital asset of the platform. It lays out a feedback loop in which platform revenue buys and burns VVV, supply falls, and the token becomes scarcer.

Staking VVV also mints DIEM, a credit equal to one dollar of daily-renewing Venice compute access.

Erik Voorhees framed the round on X as “VVV and Capital,” explaining that Venice funded growth with equity while its treasury VVV holdings stayed untouched.

He said Venice still holds more VVV than anyone else, more than 30 million tokens out of upward of 80 million in supply. Neither Venice nor its team has sold VVV despite the token's rally this year.

Venice plans to build its own compute infrastructure, including its first data center, cutting reliance on leased GPUs. Voorhees said the resulting margin improvement could make larger VVV burns feasible: better margins fund more revenue capacity, and more revenue capacity funds bigger burns.

The equity and token disconnect

Dankrad Feist offered a skeptical take, saying that the token-and-equity split in the deal “sucks,” since equity holders have legal protections while token holders depend on Venice continuing its buybacks and burns.

The criticism lands because Venice itself markets VVV as the platform's capital asset, a framing that leads token holders to expect to be close to the company's economics.

Both sides agree that Venice is a real business with real revenue and that revenue continues to expand, and the disagreement is over which asset captures it.

Equity holders own a legal claim on Venice AI, backed by a contract, while VVV holders own a designed economic claim, built from staking, DIEM, and a burn mechanism that depends on Venice choosing to keep running it.

Equity holders have legal ownership of Venice AI and the governance rights specified in their deal documents. VVV holders receive staking access, a DIEM minting path, exposure to the buy-and-burn mechanism, and the ability to trade the token on open markets.

Series A investors, through their VVV grant and warrants, now hold a slice of both layers at once.

The $1 billion equity valuation implies a roughly 14.3x multiple of Venice's reported annual revenue. VVV trades around $13.55, putting its market cap near $637 million and its fully diluted value near $1.54 billion, or about 9.1 times and 22.1 times revenue on those two measures.

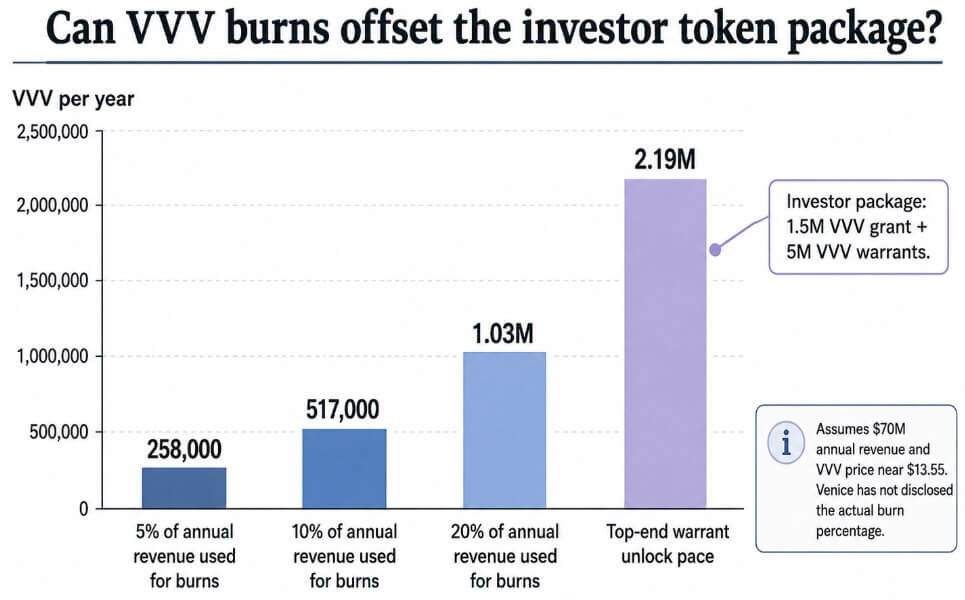

Whether burns can offset the new token supply depends on a burn percentage that Venice has kept undisclosed. At 5% of annual revenue, Venice would retire roughly 258,000 VVV per year at current prices, climbing to 517,000 and 1.03 million at 10% and 20%, respectively.

The investor package alone carries 6.5 million VVV in grants and warrants, with the grants and warrants phased in over a one-year lock and three years of vesting.

Voorhees has estimated that fully exercised warrants would add fewer than 6,000 VVV a day to circulation once they start unlocking, a pace of roughly 2.19 million VVV a year at the top end.

Goldman Sachs projects $765 billion in AI capital spending in 2026, climbing to $1.6 trillion by 2031, and compute buildout of that size tends to reward hardware owners over companies that lease.

Raising equity for GPUs and a data center is a standard move for a company at Venice's stage. Keeping VVV as the public economic layer on top of that equity round is the part of crypto that's still being argued about.

How this plays out

In the bull case, Venice turns the equity raise into computing ownership fast enough to widen margins within the next year or two.

Annual revenue keeps climbing past the current $70 million run rate, buy-and-burn volume grows with it, and VVV's token-linked dilution from the Series A grant and warrants ends up smaller than what burns retire.

Venice keeps its position as the largest VVV holder, and the token starts trading like a credible claim on the platform's growth.

In the bear case, Venice's equity value outruns VVV's. The company keeps expanding, compute investment pays off, and most of that upside flows to equity holders through a valuation multiple that the token cannot match.

Burns stay modest relative to VVV's $1.54 billion fully diluted value, and the Series A warrants unlock on schedule. The market starts pricing VVV as an access asset for staking and DIEM, a narrower role than a full claim on Venice's enterprise value would carry.

| Scenario | What happens | Who captures most value | What it means for VVV |

|---|---|---|---|

| Bull case: token captures the flywheel | Equity funds compute ownership, margins improve, revenue grows, and larger burns reduce VVV supply faster than token-linked dilution expands it. | VVV holders and equity holders both benefit | VVV trades like a credible revenue-linked asset. |

| Base case: two layers coexist | Venice grows, but VVV remains mainly a staking, DIEM, and burn-exposure asset rather than a direct company proxy. | Split between equity and token holders | VVV works, but at a discount to equity because rights are weaker. |

| Bear case: equity outruns token value | Venice becomes more valuable as a company, but burns remain modest relative to FDV and investor warrants unlock over time. | Equity holders | VVV is repriced as an access asset, not a full claim on Venice’s growth. |

| Black swan: token role weakens | Future strategy, regulation, or financing choices reduce VVV’s importance to the platform. | Equity holders | VVV loses the “capital asset” narrative and trades mostly on utility. |

Venice already did the hard part that crypto claims to want: build a real product, generate real revenue, launch a public token, and raise outside capital only then.

Every dollar Venice adds to its revenue makes it more urgent to know whether that dollar shows up in VVV's price, in Venice AI's equity value, or is split unevenly between the two.

The post Venice’s $65M raise makes VVV holders ask how much of Venice’s growth reaches the token appeared first on CryptoSlate.