XRP cleaned out leverage, now ETF demand has to prove itself

XRP’s late-June washout removed a major source of market instability: excess leverage that could have turned another sharp move into a liquidation cycle. The next test is harder because XRP now needs ETF and spot buyers to carry the market without rebuilding the same crowded futures trade.

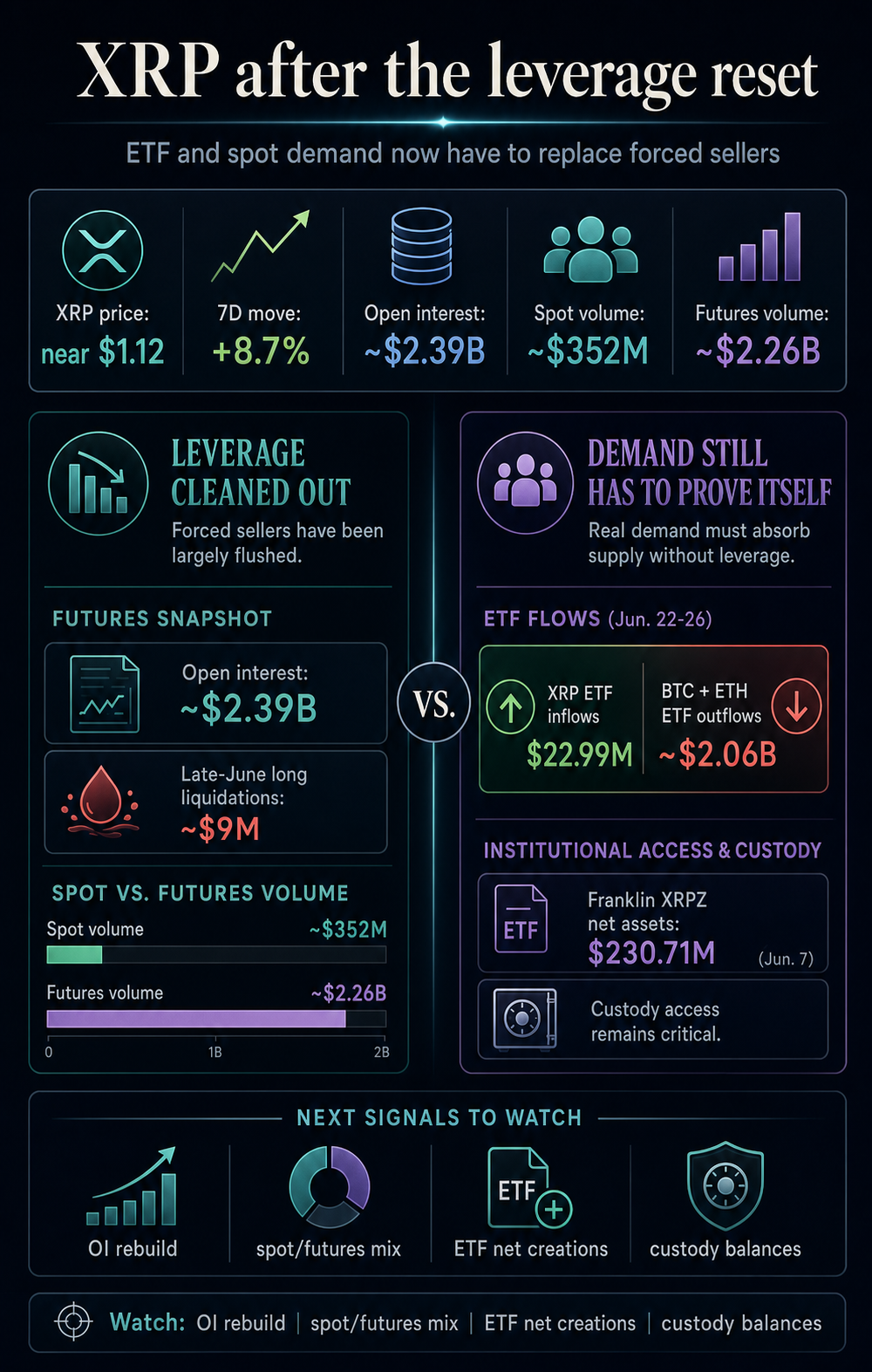

The rebound is now a test of real demand. XRP has moved away from the pressure zone that defined the late-June washout, when prior CryptoSlate coverage showed the token falling to $1.02, long liquidations accelerating, futures activity shrinking, and realized losses hitting the weakest reading since 2022.

A market can stabilize after sellers run out, but a sustained rebound requires new buyers to step in.

CryptoSlate's XRP market data shows the token trading near $1.08, up about 2.7% over seven days, with a market value of about $67 billion.

Coinglass data shows roughly $402 million in 24-hour spot volume against about $2.25 billion in futures volume, with open interest around $2.35 billion and about $8.3 million in liquidations over the prior day.

Bitcoin and Ethereum remain the main market anchors, with BTC dominance at 58.2% and ETH dominance at 9.9%.

While those numbers show XRP's setup has improved, they still don't answer the main question about demand. Futures look much more balanced than they did during the washout, although derivatives still dominate XRP's visible turnover. ETF demand has been steady in recent flow windows, but its scale remains too small to settle the question on its own.

The reset lowers risk, but demand still has to show up

Open interest provides useful context for position size by showing how many futures contracts are active in the market. It tracks contracts that traders still hold, which helps show how much leverage may still be exposed to the next price move.

CoinGlass' open-interest guide noted that falling OI can reflect forced liquidations, voluntary exits, or traders reducing exposure as volatility rises.

That range of possible causes shows why XRP's reset can cut both ways. On the bullish side, fewer crowded positions mean fewer traders are sitting at liquidation levels that can turn a normal price move into a chain of forced selling.

We've seen this happen at the end of June. XRP's drop toward $1.07 triggered about $9 million in long liquidations, and XRP open interest fell to about $2.34 billion.

Futures turnover was also down to roughly $2.84 billion from more than $30 billion during the same period last year.

That is a real reduction in speculative pressure across the XRP derivatives market. It means XRP can climb from a smaller pile of leveraged long positions. A smaller rally from that base can be healthier because fewer distressed positions are being closed into every bounce.

The bearish case is that a lower-risk setup still needs a demand engine. If open interest stopped expanding because traders lost conviction, the absence of forced sellers could be what creates temporary relief.

The market still needs a replacement buyer, and the obvious candidates are spot traders and ETF allocators.

The current numbers keep the picture balanced. While spot volume is meaningful, futures volume still represents a much larger share of XRP's visible trading activity in CoinGlass data.

Liquidations have moved out of the main headlines, but open interest remains large enough for XRP to become a leverage-driven trade again. That risk increases if traders rebuild positions faster than spot demand improves.

That leaves a practical hurdle for any sustained move. XRP can coexist with active derivatives markets, but it needs spot buying and ETF allocations to expand while leverage stays contained.

A bounce driven mainly by lower liquidation pressure can give the market time to stabilize. However, sustained strength requires buyers who can absorb future selling from holders waiting to exit near cost.

ETF demand has been steady, but scale is the caveat

The stronger case for a healthier XRP market comes from regulated products that have continued to draw selective interest during broader risk-off periods. These products are an important part of the market because they represent demand outside the high-leverage futures trade.

CryptoSlate's recent institutional-flow coverage showed that from June 22 to June 26, U.S. spot Bitcoin ETFs lost about $1.79 billion and U.S. Ethereum ETFs lost about $273.5 million.

XRP spot ETFs took in $22.99 million during the same period. That flow was directionally important because it showed XRP products gained assets while the largest ETF complexes saw outflows.

However, it's important to note that the signal also came at a limited scale, because XRP's $22.99 million inflow sat beside roughly $2.06 billion in combined Bitcoin and Ethereum ETF outflows.

That stops short of a wholesale rotation into XRP, but it points to selective buying in a market where institutions were still cutting broad crypto beta.

CoinShares' June 1 fund-flow report carried a similar message. Digital asset investment products saw $1.67 billion of outflows, with Bitcoin losing $1.438 billion and Ethereum losing $257 million.

XRP was one of the few altcoins with meaningful positive demand, drawing $20.3 million. Again, the signal was positive, while the scale was modest compared with the capital leaving the largest assets.

The ETF inflows carry weight because they represent a different type of exposure from leveraged futures positions.

The Franklin XRP ETF S-1 says the fund is passive, seeks to reflect the price of XRP before expenses, and will avoid leverage, derivatives, or similar instruments.

Franklin's launch release said XRPZ is structured as a grantor trust that holds XRP, with Coinbase Custody Trust Company serving as XRP custodian. The product page listed total net assets of $230.71 million as of June 7.

Grayscale's GXRP page uses a similar passive framing, saying the fund is solely and passively invested in XRP. It also states that the fund seeks to reflect the value of XRP held by the trust, less expenses and liabilities.

There is a straightforward reason ETFs could provide stronger long-term support for XRP. ETF demand is much steadier than high-leverage futures activity because it moves through brokerage accounts, custody arrangements, and fund-share creation mechanics.

If allocations keep arriving, they can absorb XRP supply without depending on traders borrowing to make directional bets.

ETF demand becomes a dominant price force only when net creations are persistent enough to go against the rest of the market. Those creations are important because they indicate when ETF demand requires that underlying XRP enter the fund wrapper.

CryptoSlate's earlier ETF analysis separated AUM from fresh buying because AUM can rise for several reasons. It can increase when price rises, when seed inventory exists, or when investors trade ETF shares with each other.

Net creations give a much better signal because they show the part of the ETF process that requires new XRP purchases. That makes them a more useful measure of direct ETF demand than AUM alone.

What would make XRP's move durable?

The next phase for XRP depends on whether a different buyer base is willing to take over after the worst of the wipeout.

| Signal | Healthier signal | Weaker signal |

|---|---|---|

| Futures open interest | Stable or slowly rising while the price holds | Fast rebuild that recreates liquidation risk |

| Spot versus futures volume | Spot volume expands relative to derivatives | Rallies remain mostly futures-led |

| ETF flows | Positive net inflows continue through weak market days | AUM holds up, but net creations fade |

| Custody balances | ETF holdings keep absorbing supply | Custody growth stalls while price relies on leverage |

A healthier XRP move can happen alongside active futures trading because liquid derivatives markets are normal for large tokens.

What would matter is balance: open interest that does not outrun spot buying, ETF flows that remain positive across several reports, and custody balances that show shares are backed by real XRP accumulation rather than secondary-market churn.

The available data is insufficient to prove that XRP's rally is mostly short covering, though it shows why that explanation remains plausible enough to watch.

If price rises while futures volume dominates and open interest looks driven by position cleanup rather than fresh spot demand, the rally would be less convincing. If price holds while ETF inflows continue and spot volume improves, the market would show a stronger buyer base.

The most important shift is psychological. During the capitulation phase, XRP's market was defined by traders who wanted to sell. After the wipeout, it's defined by who actually wants to buy.

ETF demand and spot accumulation can answer that question when they appear in the data with enough persistence and scale. The flows need to be large and consistent enough to matter against futures activity and spot selling.

For now, XRP's market structure is cleaner than it was during the late-June stress, which gives it a better starting point.

The next leg still has to show that ETF and spot buyers can provide stronger support than the relief created by the absence of forced sellers.

The post XRP cleaned out leverage, now ETF demand has to prove itself appeared first on CryptoSlate.