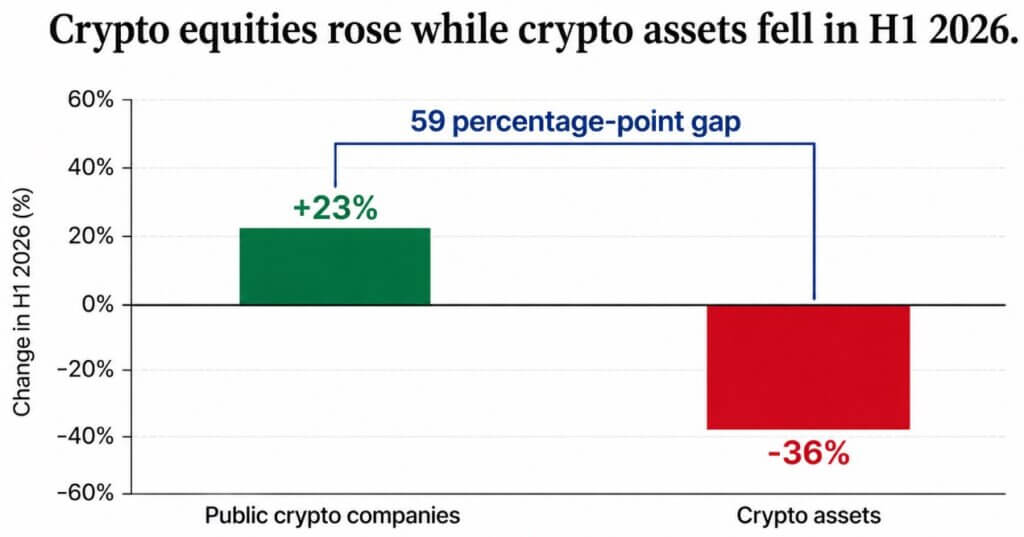

Crypto equities gained 23% while crypto tokens fell 36% this year – Is value shifting?

Bitwise reported that publicly traded crypto companies gained 23% in the first half of 2026, while crypto assets fell 36%, creating a 59-percentage-point gap.

Equities could be pricing in a recovery that sits above where the tokens currently trade, or they could also be capturing revenue crypto adoption generates for companies through fees, yield, and services that exist whether tokens rise, fall, or sit still.

Across recent crypto cycles, crypto equities and major tokens have generally moved in the same direction. When Bitcoin and other large-cap assets rallied, exchanges earned more, miners expanded, venture funding returned, and much of the industry benefited.

Whether that link still holds is one of the points Bitwise's report raised.

What the equity basket is made of

Bitwise's crypto-equity theme (BITQ) recently listed Coinbase, Strategy, IREN, BitMine, MARA, Galaxy, Figure, Cipher, Hut 8, and Riot among its top holdings.

That mix spans fee-based platforms, Bitcoin treasury companies, and miners whose valuations remain highly sensitive to BTC, so the 23% gain compresses several distinct exposures into one figure.

Stablecoins make the clearest case, as DeFiLlama puts the total stablecoin market cap near $310 billion, with Tether earning roughly $482 million and Circle roughly $193 million in 30-day revenue, mostly from yield on the assets backing their tokens.

Circle's numbers showed $653 million in reserve income last quarter, up 17% year over year, and the company just received final OCC approval to run a national trust bank.

That revenue arrives whether the person spending a stablecoin ever buys a volatile crypto asset as an investment.

Coinbase's retail derivatives revenue topped $200 million annualized in the first quarter, and its prediction market business passed $100 million annualized within two months of its US launch.

Robinhood's total net revenue grew 15% year over year to $1.07 billion in the first quarter even as crypto transaction revenue fell 47% to $134 million. Options, equities, net interest income, and $147 million in other transaction revenue, primarily from event contracts, offset the decline; customers traded a record 8.8 billion event contracts during the quarter.

TeraWulf offers the clearest version outside trading altogether, as the firm signed a 20-year data-center lease with Anthropic worth an estimated $19 billion in contracted revenue, a deal that has little to do with whether Bitcoin's price recovers.

| Growth area | Who captures revenue first? | Revenue source | Does the token need to rise? |

|---|---|---|---|

| Stablecoins | Issuers, reserve managers, payment firms | Reserve yield, payment fees, distribution | No |

| Exchanges | Public companies, market makers, custodians | Trading fees, spreads, subscriptions, custody | Not necessarily |

| Prediction markets | Platforms, exchanges, liquidity providers | Fees, spreads, event-contract volume | No |

| Tokenization | Issuers, custodians, transfer agents, infrastructure firms | Issuance, servicing, custody, settlement | Only if token captures fees |

| Mining / AI data centers | Public miners, power-site owners, AI customers | Hosting revenue, leases, compute contracts | No |

| Ethereum / Hyperliquid-style tokens | Token holders, validators, protocol funds | Fee burn, staking yield, buybacks | Yes, if mechanism works |

The mechanisms that give tokens a claim

Ethereum burns a portion of every transaction fee, directly tying network usage to a shrinking token supply, and Hyperliquid routes most of its fees into a fund that buys back its token.

Those mechanisms create a pathway for network activity to affect token supply or demand. Stablecoins generally do not pass reserve income to holders, whereas exchange shareholders capture the company's economics through equity rather than through a protocol token.

The numbers for the second quarter also complicate a purely bearish read, with Bitwise's Crypto Innovators 30 Index climbing 30.6% in the quarter.

Its large-cap crypto index fell 15.4% over that same period, and prediction market volume hit $43.2 billion with tokenized real-world assets climbing toward $33 billion.

Usage kept expanding through the same stretch the tokens fell, which is what the lagging-assets explanation would predict too.

Treasury Secretary Scott Bessent said in June that stablecoins, tokenization, and new payment systems will shape the future of money, language that treats this infrastructure as dollar plumbing more than crypto speculation.

Research cited by the ECB found that a $3.5 billion inflow into dollar-backed stablecoins can lower three-month Treasury bill yields by roughly 2.5 to 3.5 basis points, evidence that stablecoin growth is already touching traditional rates markets on its terms.

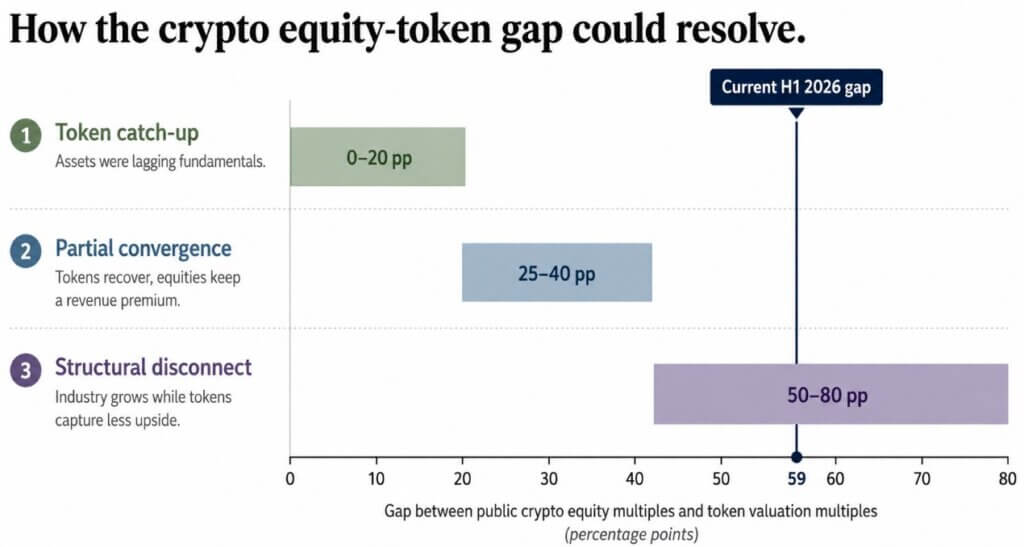

How the gap resolves from here

If risk appetite returns and ETF flows improve, DeFi and app revenue could start translating into fee burns, staking rewards, and buybacks that reach token holders directly. A broad recovery in Bitcoin and other major assets would narrow the divergence, although the size of that change would also depend on how crypto equities perform.

That outcome would mean the old adoption thesis still works for the assets built with a real value-capture mechanism attached.

If stablecoins, exchanges, tokenization platforms, and AI-linked miners keep expanding while Bitcoin, Ethereum, and most altcoins remain weak, the divergence could persist or widen beyond the 59-percentage-point gap recorded in the first half.

A chart shows three possible paths for the crypto equity-token gap: token catch-up, partial convergence, or a persistent structural disconnect.That outcome means crypto keeps succeeding as an industry, with a large share of its tokens failing to capture any of that success.

The numbers for the first half point out that crypto can build real businesses. The open question is whether the tokens investors bought to own that growth carried any real mechanism to capture it, or whether the industry found a way to keep the profits and let the assets watch from the sidelines.

The post Crypto equities gained 23% while crypto tokens fell 36% this year – Is value shifting? appeared first on CryptoSlate.