Robinhood tackled Coinbase head-on then immediately inherited Base’s biggest problem

Coinbase is reshaping its Ethereum layer-2 network, Base, around trading, payments and tokenized assets as Robinhood’s new blockchain rapidly gains users and liquidity in many of the same markets.

On July 15, Base creator Jesse Pollak acknowledged that the network’s earlier emphasis on social products had allowed it to lose ground in several of crypto’s fastest-growing financial categories.

Pollak wrote on X:

“The entire social side of the market that many of us had been building towards — Farcaster, Zora, mini apps, and yes, creator coins — disintegrated completely.”

Base will now concentrate on trading, payments and tokenized assets, bringing Coinbase into closer competition with companies building blockchain infrastructure for financial settlement.

Pollak identified Robinhood and Stripe as formidable rivals as both expand their roles in tokenization and stablecoin payments.

Base loses ground during its social push

Over the past years, Base had bet that Farcaster, Zora, mini apps and creator coins could form the foundation of a consumer-focused crypto economy.

The strategy sought to turn posts, profiles and other online content into tradable assets, allowing creators to develop direct financial relationships with their audiences.

The model initially generated substantial activity. At its peak, Base became the leading blockchain for daily token launches, briefly overtaking Solana for the first time since 2023 as users created and traded large numbers of content and creator coins.

However, that momentum proved difficult to sustain. Interest in social tokens weakened as developers, users and capital moved toward stablecoins, perpetual futures, prediction markets and other products with clearer financial uses.

The downturn exposed a widening divide between the areas Base had emphasized and those attracting more durable activity across the industry. Artemis data showed that daily users on Base fell sharply from their mid-2025 peak even as capital continued to accumulate in the network’s financial applications.

In view of this, Pollak acknowledged that Base made insufficient progress in tokenization and enterprise payments as exchanges, fintech companies and financial institutions increased their focus on those markets.

He wrote:

“We realized how our focus on social had meant that Base had fallen behind in key areas that were now increasingly critical.”

Base is responding to this situation by separating the development of its consumer app from the underlying blockchain's strategy.

Pollak has returned oversight of the Base app to Coinbase, where Jordan Fish, the crypto investor known as Cobie, will lead its development. Pollak will concentrate on positioning the network as settlement infrastructure for global financial activity.

Fish founded Echo, an onchain fundraising platform that Coinbase acquired for about $375 million in October 2025. Echo had facilitated more than $200 million across roughly 300 deals before the purchase.

Coinbase said at the time that Echo could help it expand beyond token fundraising into tokenized securities and other real-world assets. The handoff places Fish in charge of the user-facing product while Pollak focuses on Base’s infrastructure and developer ecosystem.

Robinhood Chain gains early advantage

As Base resets its strategy, Robinhood's new blockchain is experiencing an unusually fast start.

Robinhood Chain, an Ethereum layer-2 network built using Arbitrum technology, was designed to support tokenized securities, lending, decentralized exchanges and other financial applications. Transactions are processed on the network and settled through Ethereum.

Robinhood opened the network to the public on July 1 with support from Uniswap, Chainlink, and BitGo. It also introduced stock tokens that eligible customers in more than 120 countries can trade around the clock through Robinhood Wallet and decentralized exchanges.

These products helped draw early interest to the network, particularly among Robinhood’s existing international user base.

By offering around-the-clock access to tokenized equities through familiar interfaces, the company was able to channel trading activity onto its blockchain more quickly than a network launching without a built-in distribution channel.

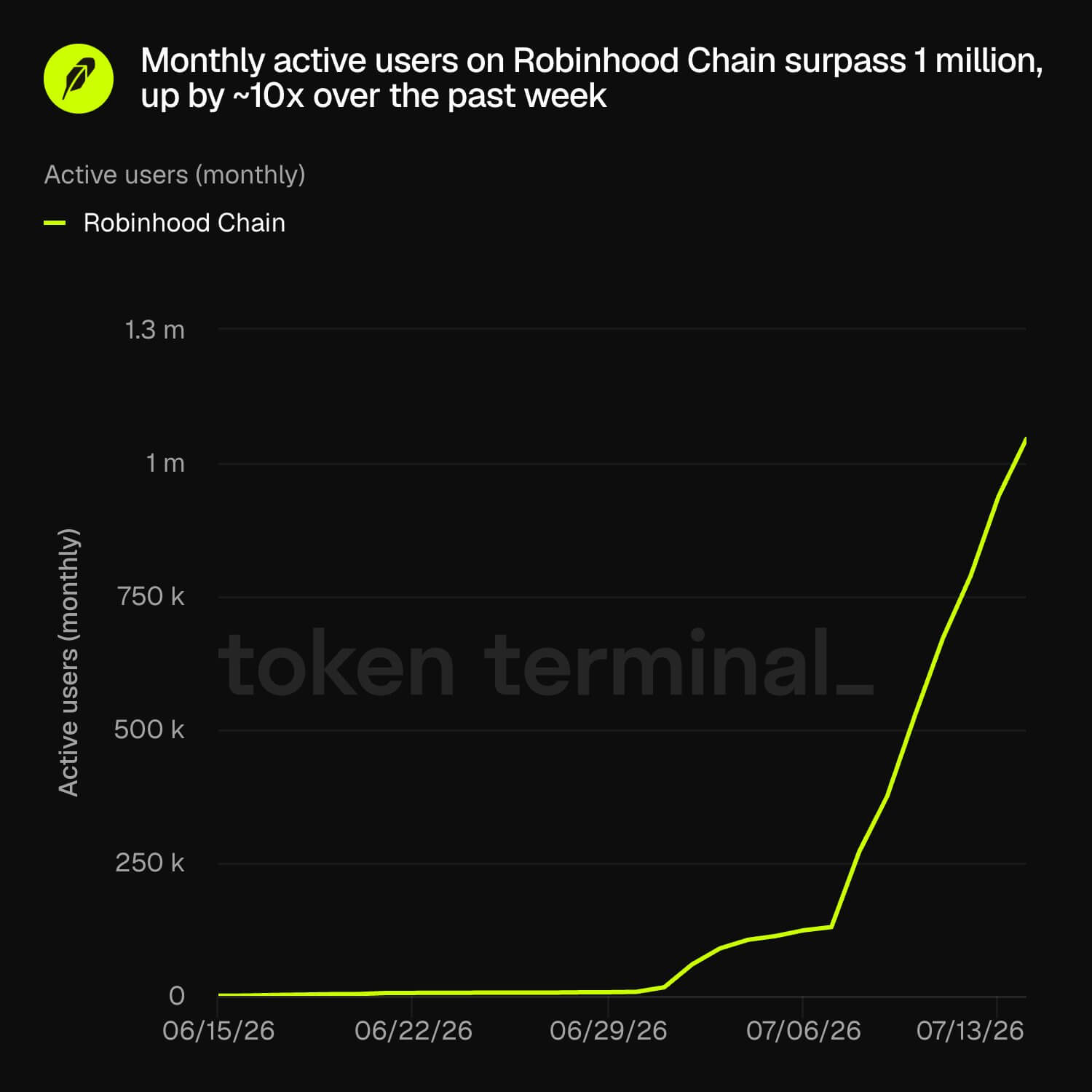

As a result, monthly active addresses on Robinhood Chain increased roughly tenfold in one week to more than 1 million, Token Terminal said. The network also briefly overtook Base in daily transactions about 10 days after its launch.

At the same time, more than 62,000 unique addresses held stock or exchange-traded fund tokens on Robinhood Chain within about two weeks, representing 11.1% of addresses holding tokenized stocks across the broader market, Token Terminal said.

Trading activity expanded alongside adoption of the stock products. Decentralized exchanges on Robinhood Chain handled about $3.1 billion over seven days, according to DeFiLlama data. This places the network among the leading blockchains for spot trading during the period.

Stablecoin supply surpassed $300 million, while integrations with Morpho, Ethena and Uniswap helped direct capital into lending and trading applications.

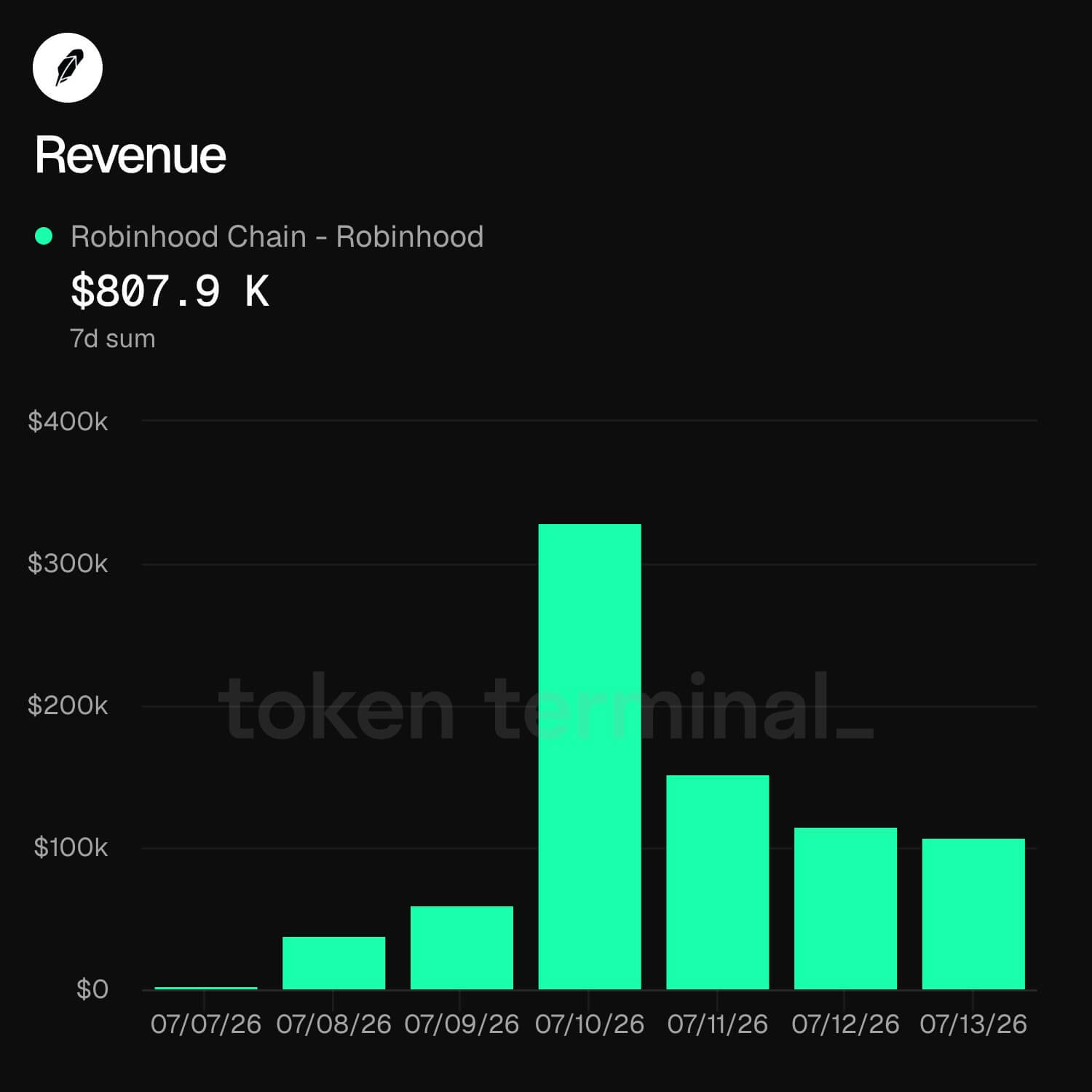

This early activity has also begun generating revenue. Robinhood Chain produced more than $800,000 over seven days, Arbitrum said. That would equal about $42 million annually if the pace continued.

While the early figures remain too limited to demonstrate lasting adoption, they still show how Robinhood has compressed tokenized assets, lending and decentralized trading into a branded financial network.

Memecoins complicate Robinhood’s early lead

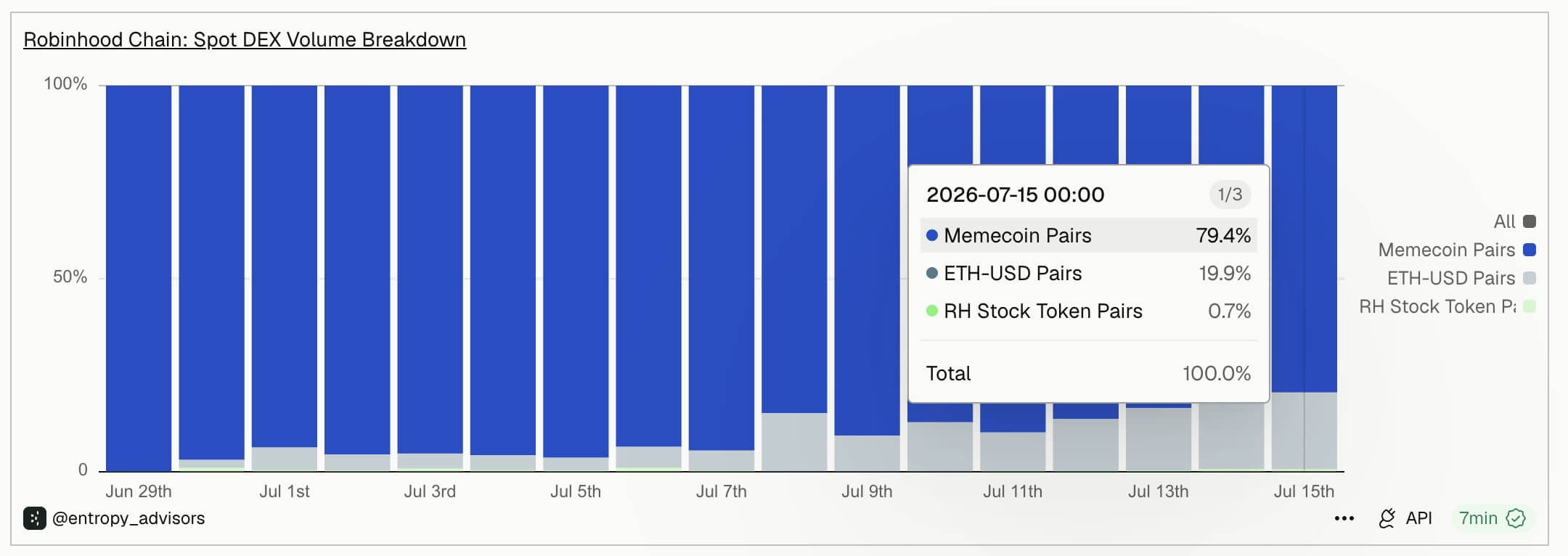

Robinhood’s early lead becomes less clear when the activity is broken down, with memecoins accounting for far more trading than the financial assets the network was built to support.

Tom Wan, head of data at Entropy Advisors, estimated that memecoins accounted for about 80% of spot trading on decentralized exchanges on Robinhood Chain.

The concentration suggests that much of the network’s rapid transaction growth has come from traders rotating through volatile tokens rather than investors moving sizable stock portfolios onchain.

CASHCAT became the clearest expression of that demand. The cat-themed token, named after an early Robinhood mascot, reached a market value of about $150 million during its initial rally.

That was more than 10 times the combined value of tokenized stocks held on Robinhood Chain at the time, illustrating the gap between the network’s stated real-world asset strategy and the activity driving its early growth.

The pattern echoes Base’s own development. Memecoins and trading applications helped attract users after Coinbase launched the network in 2023, before more durable activity formed around stablecoins, decentralized exchanges and lending.

Base later placed greater emphasis on social products and creator tokens, triggering another burst of speculative activity that failed to sustain demand.

Robinhood faces a similar situation and an added reputational risk because of its role in the 2021 meme-stock boom. Allowing memecoins to dominate its blockchain could reinforce Wall Street’s view of the company as a venue for speculative retail trading rather than a serious platform for tokenized finance.

Jon Ma, co-founder and CEO of blockchain data company Artemis, noted that while memecoins can quickly generate users and fees, losses from short-lived tokens risk eroding trust and making it harder for Robinhood to establish the longer-term financial products at the center of its blockchain strategy.

Base and Robinhood converge on the same financial markets

Coinbase and Robinhood are now left to confront the same challenge of converting their distribution advantages into lasting financial demand.

Coinbase began as a cryptocurrency exchange and has expanded into payments, derivatives, fundraising, tokenized assets and machine-driven commerce. Base gives the company a blockchain on which those products can be issued, traded and settled.

Pollak revealed that Base will organize its next phase around trading, payments and artificial intelligence agents.

The trading strategy will span tokenized stocks, memecoins, application tokens and other crypto-native assets. Its payments push will focus on making stablecoins easier for consumers and businesses to use across borders.

Base also plans to support AI agents that can hold and spend cryptocurrency, reflecting Pollak’s view that autonomous software will become a growing class of economic participant.

According to Pollak, these efforts are geared towards building “Base into the blockchain for global finance” and “the place that the world’s money settles over the next century.”

Robinhood is approaching the same opportunity from traditional brokerage. The company is using blockchain infrastructure to extend trading hours, introduce self-custody and lending, and give international customers access to assets linked to US markets. Robinhood Chain gives it greater control over the infrastructure connecting those services.

However, the company must move users away from the speculative tokens that drove much of its opening volume toward the stock tokens, lending markets, and payment products the network was designed to support.

Ma argued that Robinhood could earn up to $10 billion in revenue from such a focus if its business grows to serve 100 million monthly users and generates an average annual revenue of $100 in annual revenue per user.

According to him, this would make Robinhood Chain become a gateway for international customers seeking tokenized stocks, stablecoins, prediction markets, and exposure to private companies.

However, that scenario rests on aggressive assumptions. Robinhood would need to expand far beyond its existing customer base while maintaining meaningful revenue per user across markets with different regulations, fees, and trading behavior.

The post Robinhood tackled Coinbase head-on then immediately inherited Base’s biggest problem appeared first on CryptoSlate.