This Bitcoin-backed company is betting retiring founders will swap private stock for their life’s work

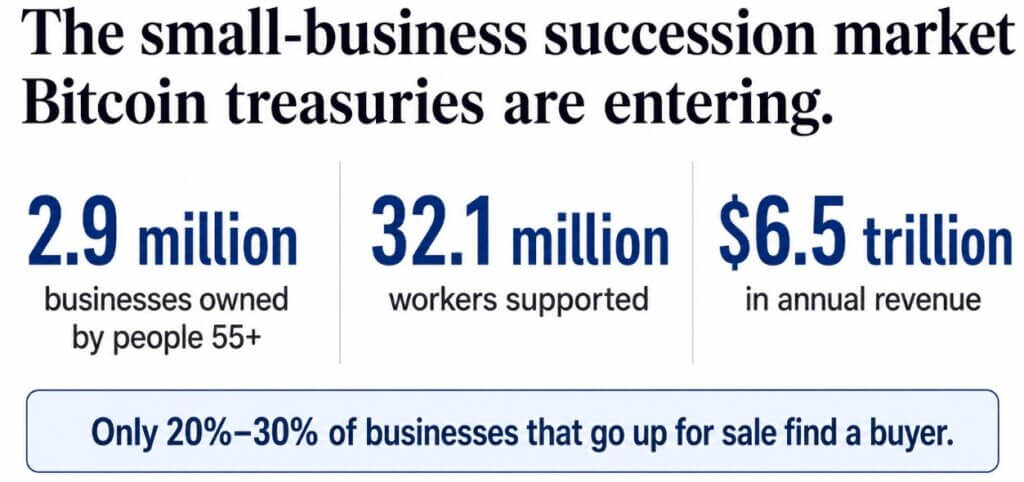

Roughly 2.9 million American businesses are owned by people 55 or older, supporting 32.1 million workers and generating $6.5 trillion in annual revenue, according to research from Project Equity and Harvard Business School.

Only about 20% to 30% of businesses that go up for sale find a buyer at all, per the Exit Planning Institute.

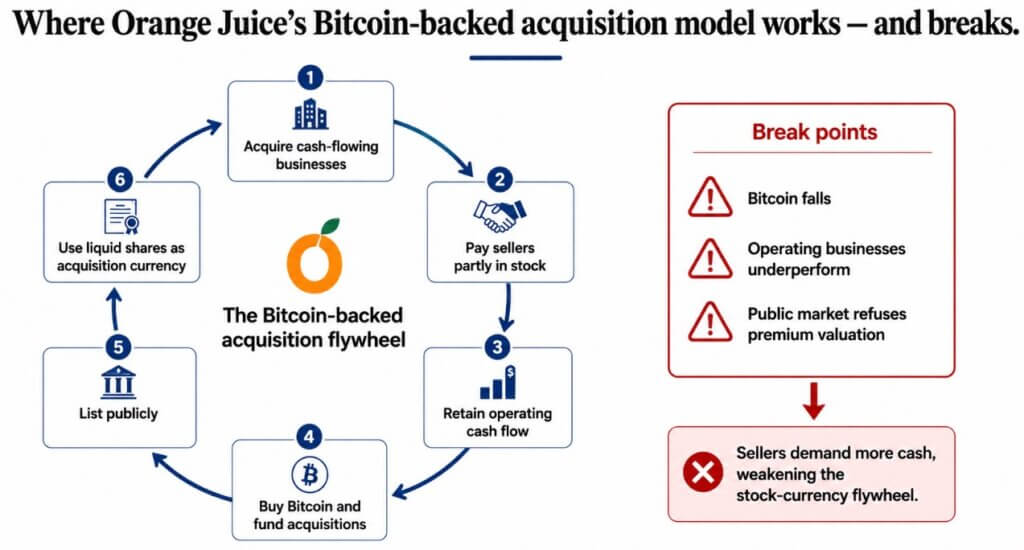

Orange Juice Holdings Inc. wants to become one of those buyers, with the additional plan to acquire cash-flowing businesses generating $1 million to $10 million a year, hold them permanently, pay sellers partly in Orange Juice stock, and put some of the retained earnings toward Bitcoin.

Orange Juice is a newly launched Connecticut permanent-capital holding company. It was founded by ego death capital partners Jeff Booth, Lyn Alden, Nico Lechuga and Andi Pitt, alongside Adrian Steckel, with Ruben Zweiban running day-to-day operations. Mexican billionaire Ricardo Salinas participated as the anchor investor.

The company raised $40 million to acquire and permanently own cash-flowing American businesses while building a Bitcoin treasury.

A different buyer for a familiar trade

The Bitcoin treasury model that made companies like Strategy famous runs through public markets.

The company issues shares to raise capital, uses the proceeds to buy Bitcoin, and its stock then trades at a premium or discount to the value of the Bitcoin it holds. That entire loop happens between the company and public market traders who choose to buy in.

Orange Juice's version runs on a founder who sells their business, takes part of the payment in cash and part in Orange Juice stock, and whose operating cash flow helps fund both future acquisitions and Bitcoin purchases.

Orange Juice plans to use private shares in acquisitions before a listing, while an eventual public listing could make the stock more liquid and easier to use as acquisition currency at scale. The listing remains a stated goal, with its timing still undecided.

A retiring plumbing company owner or regional manufacturer accepting Orange Juice stock as part of their payout may be taking on the same exposure as a condition of selling the business they spent decades building.

Once they accept stock, they own a minority stake in a holding company built from businesses chosen by someone else, run by managers who answer to someone else, and subject to Bitcoin's price swings on top of everything else.

Orange Juice's materials describe the future public listing as a goal it's working toward, which means seller equity today functions purely as a private-company claim.

| Before sale | After accepting Orange Juice stock |

|---|---|

| Concentrated ownership in a business the founder built | Minority ownership in a holding company assembled by someone else |

| Control over management, capital allocation, and timing | Exposure to decisions made by Orange Juice management |

| Familiar operating risk in one company or region | Diversified operating risk across acquired businesses |

| Wealth tied to business cash flow and sale value | Wealth tied to Orange Juice valuation, future liquidity, and Bitcoin exposure |

| Sale value usually negotiated in cash or debt-financed consideration | Part of the payout may depend on private stock that is not yet publicly liquid |

| Succession risk: finding the right buyer | Post-sale risk: whether the buyer’s broader flywheel works |

The flywheel and where it can break

The mechanism has a sequence consisting of acquiring cash-flowing businesses, paying part of the price in stock, retaining cash flow to fund more acquisitions and Bitcoin purchases, building the treasury, listing publicly, then using the newly liquid shares to buy the next round of businesses.

If Bitcoin falls, if acquired businesses underperform, or if public markets refuse to value the company at a premium upon listing, seller stock becomes far less attractive.

The flywheel built around stock as currency gets harder to sustain under those conditions.

Galaxy has described the standard Bitcoin treasury playbook as a premium-to-NAV loop in which companies trade above the value of the Bitcoin they hold, raise equity at that premium, buy more Bitcoin, and use the resulting narrative to sustain the premium.

Galaxy also warned that the loop turns dangerous once the premium disappears, since issuing equity near net asset value stops adding value and starts diluting it.

Many digital asset treasury companies have already hit that wall, trading below net asset value as token prices fell, with Strategy itself selling roughly $218 million of Bitcoin this year to fund dividends and rebuild dollar reserves.

Orange Juice's operating businesses give it a cash-flow source unique among treasury-style companies. The acquisition-currency component of its plan still relies on the same kind of public market valuation that is currently under strain elsewhere in the category.

Two ways the model plays out

If Orange Juice's operating businesses perform well and public markets eventually value the company at a premium upon its listing, sellers gain confidence to accept more stock and less cash per deal.

That would let the flywheel run as designed, with equity buying businesses, businesses funding Bitcoin and further acquisitions, and the expanding treasury supporting the stock's value in turn.

If Bitcoin weakens or the eventual listing draws a skeptical market, sellers start demanding more cash and less stock, and the acquisition-currency piece of the model stalls.

Orange Juice would still be able to buy companies, just at the higher, all-cash cost the model was built to avoid.

Orange Juice is testing whether a retiring founder will accept a slice of Bitcoin-linked equity as part of the price for handing over a business they built, and whether enough of them say yes to make the model work at all.

The post This Bitcoin-backed company is betting retiring founders will swap private stock for their life’s work appeared first on CryptoSlate.