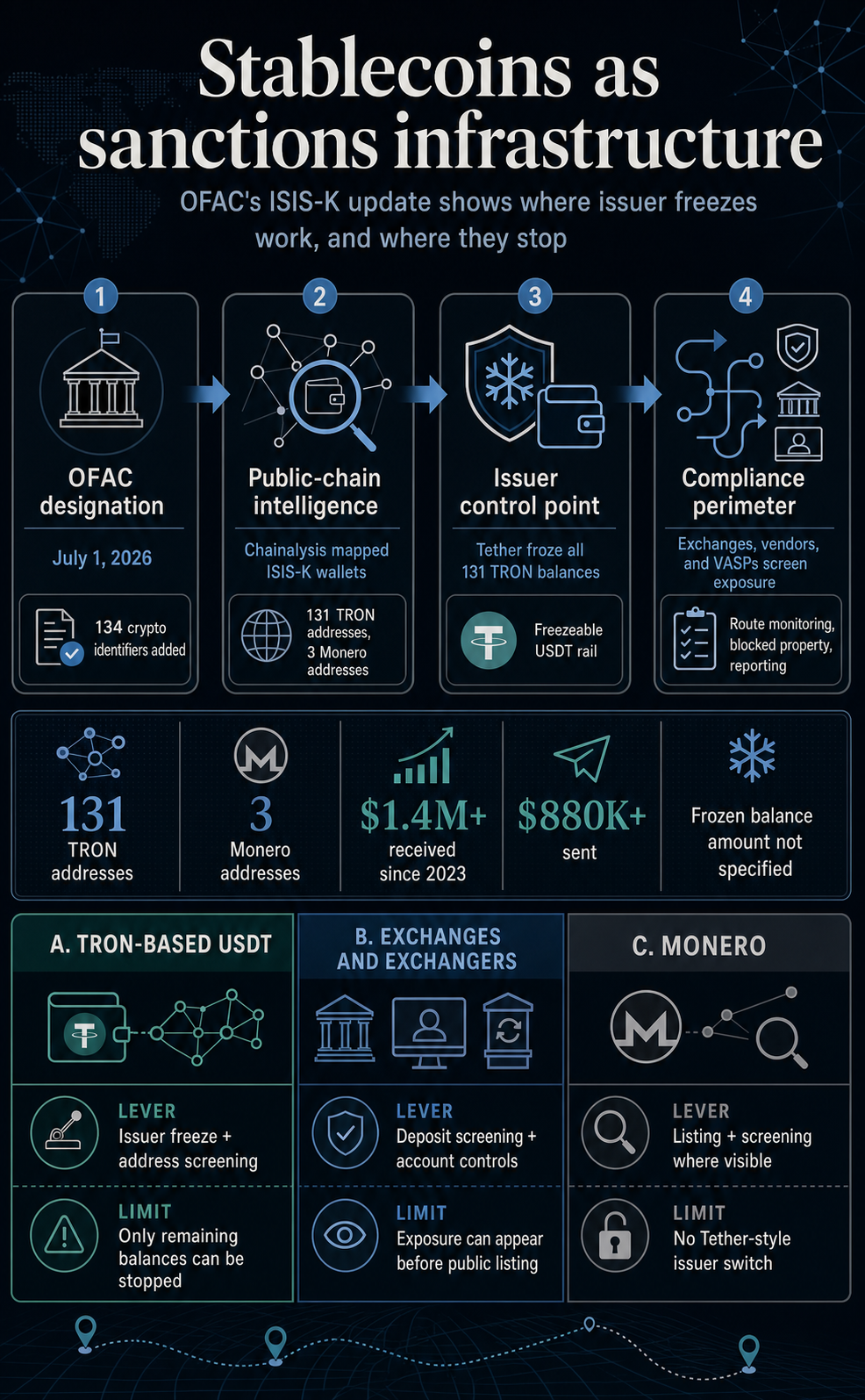

Tether freezes 134 ISIS terror wallets as stablecoins now sit inside the sanctions machine

ISIS-K, the Islamic State affiliate active across Afghanistan, Pakistan, and parts of Central Asia, had USDT balances frozen on 131 TRON addresses after an OFAC sanctions update, creating an enforcement test for stablecoins. Once public-chain intelligence, a sanctions list, and issuer controls were in place, Tether could freeze the balances within its own token system.

The July 1 action updated the ISIL Khorasan designation with digital-currency identifiers. Chainalysis said OFAC added 134 crypto addresses, including 131 TRON addresses and three Monero addresses.

It also said Tether froze the balances on all 131 TRON addresses.

The outcome turns a sanctions entry into a map of who can stop the flow of money. Governments identify a target; blockchain intelligence maps the wallets; exchanges and compliance vendors screen for exposure; and a freezeable issuer can interrupt balances within its token system.

Chainalysis said the 131 TRON wallets controlled by ISIS-K had received more than $1.4 million since 2023 and sent more than $880,000. Those figures do not show how much remained in the wallets when Tether froze them, and they should not be treated as the frozen balance.

But the flow totals show the enforcement model in action. The wallets were more than symbolic identifiers on a list. They were part of an on-chain funding route that touched mainstream services and could be screened after designation.

Stablecoin sanctions now have an issuer switch

OFAC has treated digital-currency addresses as sanctions identifiers for years, but stablecoins add a control point that does not exist in the same way for every crypto asset.

OFAC’s virtual-currency guidance says it may add digital-currency addresses to the SDN List and that parties identifying blocked digital currency should block the property and report relevant information.

For an exchange, custodian, payment firm, or compliance vendor, that means screening the listed addresses and related exposure. For a stablecoin issuer, it can also mean disabling the token balance at the contract or issuer-control layer.

Tether had already moved toward that posture. In December 2023, the company said it had introduced a voluntary wallet-freezing policy for activity related to individuals on OFAC’s SDN List.

The ISIS-K case shows what that policy means in practice when the asset sits on a transparent chain with a large USDT footprint.

The result is a different kind of sanctions perimeter. Traditional sanctions often work through banks, correspondent accounts, payment processors, and custodians. In this model, the stablecoin issuer sits closer to the asset itself.

If a listed address holds a freezeable token, the enforcement pathway can run through the issuer rather than relying only on exchanges to reject deposits or withdrawals.

That does not make the system automatic or complete. It still depends on timely intelligence, accurate labeling, legal process, operational capacity, and the issuer’s willingness or obligation to act.

It also raises hard questions about private companies becoming choke points for dollar-linked tokens that circulate globally. But the ISIS-K update shows that the issuer role is no longer theoretical.

This is the policy tension stablecoin issuers now carry. The same control that lets an issuer respond to a sanctions designation can become a standing expectation from regulators, law enforcement, exchanges, and analytics firms.

Once that expectation exists, a dollar token is judged by more than reserve quality, liquidity, and redemption access. It is also judged by how fast its issuer can act when a listed wallet appears on-chain.

TRON-based USDT sits at the center of the case

The TRON address count is the detail that gives the action its shape. Chainalysis said the ISIS-K update included 131 TRON addresses, compared with three Monero addresses.

Tether’s freeze applied to the TRON side because those balances were in a token system the issuer can control.

That detail affects exchanges and payment firms because TRON-based USDT has become a common rail for fast, cheap dollar transfers. When a sanctions action names TRON addresses, the compliance burden does not stop at the listed wallets.

Firms have to ask whether they received funds from those addresses, sent funds to them, interacted with related clusters, or served customers via adjacent cash-out routes.

Chainalysis said several of the designated wallets sent funds to Syria-based crypto exchangers and had heavy exposure to mainstream services. That is where stablecoin sanctions become infrastructure rather than paperwork.

The listed address is the starting point. The real work is mapping counterparties, deposits, withdrawals, service exposure, and any linked addresses that may not yet be public.

Tether’s recent history reinforces that trend. In April, the company said it supported freezing more than $344 million in USDT in coordination with OFAC and U.S. law enforcement.

In May, it said the T3 Financial Crime Unit involving Tether, TRON, and TRM Labs had frozen more than $450 million tied to illicit crypto flows.

Those are separate actions from the ISIS-K update, but they show a repeatable pattern: analytics identify risk, public or private enforcement channels flag wallets, and the issuer freeze becomes part of the response.

The policy backdrop is moving in the same direction. In an April proposed rule, FinCEN and OFAC set out AML/CFT and sanctions compliance requirements for permitted payment stablecoin issuers, including technical capacities to block, freeze, and reject impermissible transactions.

Regulators increasingly treat stablecoin issuers as financial infrastructure with compliance duties, not just software-adjacent token companies.

| Rail | Enforcement lever | Limit |

|---|---|---|

| TRON-based USDT | Issuer freeze, address screening, exchange monitoring | Only remaining token balances can be frozen; prior flows still require tracing |

| Centralized exchanges and exchangers | Account controls, deposit screening, withdrawal blocks, reporting | Exposure may appear before a public designation or through intermediaries |

| Monero and other non-issuer assets | Sanctions listing, screening, investigative tracing where possible | No Tether-style issuer control point for freezing balances |

The Monero addresses show where the model stops

The same OFAC update also included three Monero addresses. That contrast is important because it shows the limit of issuer-driven enforcement.

Monero accounts are controlled through private keys, not by a centralized issuer that can disable a token balance. OFAC can list an XMR address, and exchanges or other covered firms can screen for exposure where they have visibility.

Investigators can still pursue leads, counterparties, devices, service providers, and user errors. But there is no equivalent of asking Tether to freeze a USDT balance at the issuer layer.

That split is likely to shape behavior. If stablecoin freezes become faster and more routine, sanctioned actors and illicit networks have incentives to shift funds toward assets or routes with fewer issuer controls.

That does not make those routes safe or invisible. It does make them harder to interrupt at a single corporate control point.

For governments, the appeal of freezeable stablecoins is obvious. Public chains leave trails. Stablecoins often touch centralized services. Issuers can act like payment processors or banks when legal and operational conditions are met.

The result is a sanctions tool that can move faster than traditional cross-border finance in some cases.

For crypto users and infrastructure providers, the tradeoff is just as clear. The same feature that lets an issuer stop funds tied to a sanctioned terrorist group also confirms that tokenized dollars carry centralized control.

That may be acceptable, even expected, for regulated payment stablecoins. It also marks a dividing line between assets designed to behave like compliant money-market infrastructure and assets designed to minimize third-party control.

That dividing line gives the ISIS-K action its forward-looking edge. The enforcement gain is strongest when illicit finance uses tokenized dollars on public chains.

The incentive to adapt is strongest when those actors can move into assets or venues where the issuer switch is absent, visibility is weaker, or cash-out points sit outside cooperative channels.

The next fight is over the route, not the wallet

The ISIS-K update points to the next phase of crypto sanctions: enforcement will focus less on a single wallet and more on the route around it.

A listed address can be frozen if it holds issuer-controlled stablecoins. It can be screened by exchanges and custodians. Its counterparties can be mapped by analytics firms.

But the funding network can still adapt by moving through new addresses, unlisted intermediaries, offshore exchangers, privacy tools, or assets without issuer controls.

The OFAC and Chainalysis record goes beyond Tether freezing 131 wallets. Stablecoin rails are becoming part of a standing enforcement stack.

The stack includes sanctions lists, blockchain intelligence, issuer controls, exchange compliance, and vendor tooling. Each part covers a different piece of the route.

The ISIS-K case also shows the model’s built-in limitation. Freezeable stablecoins are powerful when illicit finance uses tokenized dollars on transparent chains.

They are less decisive when funds have already moved, when balances are gone, when counterparties sit outside cooperative venues, or when activity shifts to assets without a centralized issuer.

For stablecoin issuers, the message is that scale now comes with enforcement expectations. For exchanges, the pressure is to detect exposure before a listed wallet arrives at the deposit page.

For compliance vendors, the value is in turning public designations into real-time routing maps. For users, the case is a reminder that the most liquid on-chain dollars are not neutral pipes. They are programmable balances inside systems that can be stopped.

The next signal will be whether actions like this remain case-by-case responses or become a normal operating layer for dollar stablecoins.

If issuer freezes, exchange screening, and chain analytics continue to converge, stablecoins will do more than just move dollars on public chains. They will help decide which on-chain dollars can keep moving.

The post Tether freezes 134 ISIS terror wallets as stablecoins now sit inside the sanctions machine appeared first on CryptoSlate.